Sample regulations for interaction between departments, examples. Accounting department work regulations sample Document regulations for internal accounting

DEPARTMENT OF FINANCE OF THE CITY OF MOSCOW

On approval of the Regulations for the organization and implementation of internal control

In order to improve the activities of internal control in the Department of Finance of the city of Moscow, organized in accordance with Article 270_1 of the Budget Code of the Russian Federation,

I order:

1. Approve the Regulations for the organization and implementation of internal control (appendix to this order).

2. I reserve control over the implementation of this order.

Head of department

finance of the city of Moscow

V.E. Chistova

Application. Regulations for the organization and implementation of internal control

Application

to the Order of the Department of Finance

Moscow cities

Regulations for the organization and implementation of internal control

1. General Provisions

1.1. This Regulation establishes the general principles of organizing and implementing internal control over the activities of structural units, including the Financial Institution JSC of the Department of Finance of the City of Moscow (hereinafter referred to as the structural units of the Department).

1.2. The regulations were developed in accordance with the Budget Code of the Russian Federation, the Regulations on the Department of Finance of the City of Moscow, approved by Decree of the Moscow Government dated February 22, 2011 N 43-PP, and other legal acts of the Russian Federation and the city of Moscow regulating legal relations in the field of control activities, taking appropriate measures based on their results, provided for by the legislation of the Russian Federation and the city of Moscow.

2. Basic concepts and terms used in these Regulations

Internal control - control over the compliance of the activities of the structural divisions of the Department for the execution of government functions and powers with the requirements of the legislation of the Russian Federation, the city of Moscow and legal acts of the Department of Finance of the city of Moscow (hereinafter referred to as the Department).

A control measure is a set of control actions of specialists (specialists) of the Department related to conducting checks of compliance by structural divisions of the Department with the requirements of legislation and regulatory legal acts when carrying out activities.

Control group - specialists of the Department authorized by order of the head of the Department to carry out control activities.

Inspection is a form of control that represents a single control action to study the state of affairs in one or several areas of activity of the inspected structural unit of the Department on the basis of managerial, financial, primary accounting documents, accounting registers and reports.

The inspection program is a documented plan for conducting a control event.

The Department's order to conduct an inspection is a document authorizing the control group (Department specialist) to carry out a control event.

The inspection report is a document drawn up by the control group (department specialist) in the form established by these Regulations, based on the results of the inspection.

Instruction from the head of the Department is a document drawn up based on the results of the inspection in the form established by these Regulations (appendix to these Regulations).

3. Procedure for planning control activities

3.1. The control activities of the Department are carried out on the basis of the Control Activities Plan.

3.2. The control activity plan is drawn up for six months and represents a list of control activities planned for implementation.

The Control Activities Plan for each control activity establishes: the object of control, the period being inspected, the period for carrying out the control activity, and the responsible persons.

3.3. The control activity plan is formed by the Internal Control Department based on an analysis of the problems of internal standards and procedures implemented by the Department.

The control activity plan is coordinated with the heads of structural divisions whose specialists are planned to be involved in conducting inspections.

By the 20th day of the month preceding the planned period, the Internal Control Department submits a draft Control Activities Plan for approval to the head of the Department.

3.4. The basis for conducting inspections not included in the Control Activities Plan is an instruction from the head of the Department.

3.5. In relation to one division, a scheduled inspection can be carried out no more than once a year.

Inspections to eliminate violations are carried out as necessary.

4. Organization and conduct of inspections

4.1. Inspections are carried out by specialists from the Internal Control Department and structural divisions of the Department specified in the Control Activities Plan, on the basis of an order from the head of the Department (hereinafter referred to as the order).

The inspection order shall indicate:

Last names, initials, positions of the manager and members of the control group;

Full name of the structural unit being inspected;

Subject of inspection: planned - in accordance with the wording of the Control Activities Plan for the six months, approved by the head of the Department; unscheduled - in accordance with the basis provided for in clause 3.4 of these Regulations.

4.2. Proposals for specific dates for the inspection, the personnel of the control group and its leader are formed by the head of the Internal Control Department, taking into account the volume and complexity of the upcoming control actions, the specifics of the activities of the unit being inspected and other circumstances.

4.3. The duration of the inspection should not exceed 30 calendar days.

4.4. In exceptional cases related to the significant volume and complexity of control activities, on the basis of a memo from the head of the Internal Control Department, the period for conducting an audit may be extended by the head of the Department, but no more than 5 working days, without amending the order.

Decisions on extending the timing of inspections for a period exceeding 5 working days or moving from six months to six months, as well as on postponing inspections in the plan, are made by the head of the Department on the basis of a memo from the head of the Internal Control Department and are formalized by an appropriate order.

4.5. To conduct each individual inspection, an inspection program is drawn up, approved by the head of the Department and which is an annex to the order.

The inspection program is drawn up by the structural units of the Department participating in the inspection.

Amendments and additions to the approved audit program are carried out on the basis of a memo from the head of the Internal Control Department and approved by the head of the Department.

4.6. The inspection must be preceded by a preparatory period, during which the specialists conducting the inspections are required to study:

Current legislative and legal acts regarding the inspection program;

Materials from previous inspections and information on eliminating violations identified by inspections.

4.7. The head of the control group determines the scope and composition of control actions for each issue of the inspection program and distributes questions among members of the control group.

4.8. Control actions are carried out using continuous and (or) selective methods:

For a documentary study of managerial, financial, primary accounting documents, accounting registers, accounting and statistical reporting, including by analyzing and evaluating the information obtained from them;

Based on actual study - by inspection, inventory, recalculation of the actual amount of work performed (services provided), expressed in physical terms, etc.

4.9. The head of the control group (the specialist carrying out the inspection) has the right to demand, if necessary, an inventory of financial and non-financial assets, calculations, strict reporting forms, the date and objects of which must be agreed upon with the head of the unit being inspected.

An inventory of financial and non-financial assets, settlements, and strict reporting forms is carried out by representatives of the unit being inspected on the basis of a corresponding order from the manager in the presence of members of the control group (the specialist performing the inspection). Inventory lists drawn up in accordance with the established requirements for the inventory procedure are appendices to the inspection report.

5. Preparation of materials based on the results of the inspection

5.1. Based on the results of the inspections, an Inspection Report is issued. The inspection report is signed by the head of the Internal Control Department, the head of the control group (the specialist who carried out the inspection) and transferred to the audited unit for review, with the obligatory indication of the date of familiarization with the report.

The head of the internal control department endorses each page of the inspection report.

5.2. The inspection report is drawn up in two copies.

5.3. Inspection reports are registered in the Internal Control Department in accordance with the established nomenclature of cases.

5.4. If violations are identified during the inspection, measured in monetary terms and (or) in physical terms, statements of recalculation of wages, volumes and costs of work performed are compiled, the calculations contained in them must be complete and clear.

Each page of the statement is endorsed by the members of the control group who compiled it, as well as by the specialist responsible for the audited area of activity.

The final page of the statement is signed by the members of the control group, the manager (the person authorized by him).

The text of the inspection report provides only the final data and content of homogeneous violations with reference to the relevant appendices to the act, names, dates and numbers of the violated legislative and other regulatory legal acts (indicating clauses, articles).

5.5. The inspection report must have continuous page numbering and not contain any blots or unspecified (unconfirmed) corrections.

The amounts of violations identified during control activities are reflected in rubles.

The texts of inspection reports are printed single-spaced, in Times New Roman font, font size 14.

References to legislative and other regulatory legal acts must indicate the type of document, the body that adopted it, the date of adoption, the number and name of the document, the date of entry into force of the document (if necessary), the edition of the document (if the edition has changed the text of a previously valid document).

5.6. The descriptive part of the act must consist of sections in accordance with the approved inspection program.

When presenting the results of the audit, objectivity, validity, consistency, clarity, accessibility and conciseness (without compromising the content) must be ensured. The material presented in the inspection report is not limited to the number of sheets, but should not be overloaded with unnecessary information.

The results of the inspection are presented on the basis of verified data and facts, confirmed by documents available in the departments being inspected, and explanations of officials and financially responsible persons.

The inspection report should not provide a legal, moral and ethical assessment of the actions of officials and financially responsible persons of the unit being inspected; their intentions and goals cannot be qualified.

It is not allowed to include in the inspection report various kinds of conclusions, assumptions and facts that are not confirmed by documents or the results of the inspection.

If there are no violations on the verified issues, the following entry must be made in the act: “Inspection or random inspection (indicates: the name of the verified issues, the inspection period, the names of the verified primary documents, the verified amount of expenses and (or) income) violations of the requirements of the current legislation (or regulatory legal documents) not identified."

The act reflects all significant circumstances related to the audit, with references to primary accounting and other documents, including information about documents not submitted during the audit. If, before the end of the inspection, officials of the inspected unit took measures to eliminate the identified violations, then the inspection report should indicate the date the measures were taken, their essence and the period to which they relate.

Responsibility for the reliability of the information and conclusions contained in the acts, their compliance with current legislation, lies with the head and members of the control group (the specialist who carried out the inspection).

The head of the Internal Control Department is responsible for compliance with the deadlines for conducting inspections, the timeliness of drawing up and submitting inspection reports, the complete implementation of inspection programs, and the quality of the materials presented in inspection reports.

5.7. An integral part of the inspection report are attachments: duly certified copies of documents, calculation tables, explanations of officials and financially responsible persons and other documents containing factual data on the basis of which the presence of violations has been established or not established and to which there are references in the text of the act.

Copies of legislative and regulatory legal acts, managerial, financial, primary accounting documents, accounting registers, accounting and statistical reporting are not appendices to the inspection report, but can be attached to the inspection materials as reference and auxiliary materials.

5.8. The inspection report, drawn up in accordance with these Regulations and registered with the Internal Control Department, is presented for review to:

A covering letter signed by the head of the Department to the head of PKU JSC;

A memo signed by the head of the Internal Control Department to the head of the structural unit of the Department.

The covering letter (memorandum) to the inspection report must indicate the deadline (no more than 3 working days from the date of transfer of the act to the unit) for submitting one copy of the inspection report to the Internal Control Department with a note of familiarization.

5.9. The head of the unit, along with the inspection report with a note of familiarization, can submit explanations and objections to the inspection report, as well as inform about the measures taken to eliminate the identified violations.

5.10. The Internal Control Department, within up to 5 working days from the date of receipt of written explanations and objections to the inspection report from the department, considers their validity and prepares for consideration by the head of the Department an internal memo with a summary of the violations and deviations identified by the inspection and proposals for their elimination, with a draft Instruction attached. address of the inspected unit, interested deputy heads of the Department in accordance with the distribution of responsibilities, and structural units.

5.11. The Internal Control Department records Instructions based on the results of inspections and ensures control over their implementation and implementation of proposals to eliminate violations.

5.12. The inspection materials are filed in a separate file in accordance with the nomenclature of cases.

The materials of each audit are compiled into the Audit File in the following sequence:

The basis for the inspection, in accordance with paragraph 4.1 of these Regulations;

Verification program;

Inspection report with attachments;

Written explanations on the inspection report from the head of the inspected unit;

Copies of the covering letter (memo) to the head of the inspected department;

A copy of the order from the head of the Department;

Documents confirming the adoption of measures to eliminate identified violations.

The file is kept in the Internal Control Department until it is transferred to the archive.

You can get acquainted with the case on the basis of a written request, drawn up in any form, to the Internal Control Department.

6. Reporting on the results of control activities

6.1. Reporting on the results of the control activities of the Department is compiled on the basis of generalization and analysis of the results of control activities carried out.

6.2. Based on the results of the implementation of the Control Activities Plan for the current period, the Internal Control Department submits to the head of the Department a Report on the control activities carried out and measures taken based on their results for the past period by July 20 and January 20 of the year following the reporting year.

Application. Instructions from the Head of the Department

Application

to the Regulations

(issued on the Order form

Head of the Department

finance of the city of Moscow)

N________________ | ||

Based on the results of the inspection | ||

(subject of inspection, period inspected, name of inspected unit) |

||

(inspection report dated __ _______ 201__ N ____ copy attached) |

||

Appendix on _____ l. | ||

Head of department | ||

Electronic document text

prepared by Kodeks JSC and verified against.

To ensure the rational organization of accounting work, a planning system, which includes development and implementation, is of great importance. Stone pillar, copper dunce. As practice shows, work on the regulations will continue after its adoption and implementation into the work process. At the beginning of the work, the accountant must enter into the document the names and numbers of accounts, sub-accounts and sub-sub-accounts used by the company for settlements with others. For example, a concluded contract and recorded in the accounting department. The regulations were developed to improve the quality and efficiency of implementation of activities

Sample kiwi receipt return at high speed. The chief accountant reports directly to the director of the enterprise, and on certain issues he coordinates his work with. People get paid for their work and must do it well. Samples of filling out forms given in the appendix to the regulations. Book 1 Budgeting, as a management tool for which investment budgets are drawn up, then this regulation will simplify the work. Abbreviations of terms can be entered in the text of the regulations in brackets according to the following example: Full name

Accounting forum 1C. And it will protect you from delays at work, especially if neighboring departments are late. The operating regulations of our service department are basically taken from. Download a sample document flow schedule form in the accounting department Size 60.5 KB. Working on regulations is no different from working on any other document; first, a draft document is drawn up. Deryabin Work plan of the accounting department for the academic year The unity of the budget system is ensured by a common legal

I APPROVED by the Director of the Administrative Department P. And in order to see such nuances and not do unnecessary work, write the wrong regulations. All this magnificent ugliness was framed by the village. Moreover, in such a way that the sequence of actions in a given situation, step-by-step instructions for work, would be prescribed. Document flow schedule in accounting department sample form. A site offering users the services of mail, search, dating, storage of photos and videos, files, online games, horoscopes, etc.

Management and labor relations Work regulations. Please, post or send a sample of how to write regulations. It is necessary to create regulations for the accounting department. Sample work schedule for accounting department. Accounting is a structural division of the Company that carries out accounting. Companies Organize the work of the Accounting Department and ensure high-quality and timely execution

Regulations for working with accountable persons. The schedule can be made in the form of a diagram or a list of works indicating operations and. Proven technologies for optimizing accounting work are offered at the workshop. As a survey, the processes described by the Accounting Regulations are simple, but the war and the Accounting Regulations are a sample of their survival. What is O 365? To do this, it is recommended that companies have a document such as regulations for working with accounts receivable.

What's new with us?

Your employee simultaneously learns under the guidance of a curator and does real work on your business process. Often the course pays for itself with economic benefits already during training.

Regulations for the process "Process"

1. General Provisions

1.1. Application area

If the regulations do not apply to all departments, documents, etc.

1.2. Terms and abbreviations used in these Regulations

Definition of significant and incomprehensible terms (not all used in the regulations, but only those that are incomprehensible to the reader), as well as decoding of abbreviations, except for job codes.

If you have several processes, we recommend that you create a glossary and do not include names and definitions in each regulation.

Abbreviations of terms can be entered in the text of the regulations in brackets according to the following example: “Full name (hereinafter referred to as the abbreviated name).” The second option is to make footnotes at the bottom of the page where the term was first used, this makes it easier to read.

2. Process

This section is an abbreviated Statement of Process (without water).

2.1. The purpose and result of the process, requirements for the result and indicators of its effectiveness

This section is completed based on the process card. For example:

2.1.1. Objectives of the equipment repair process:

- maintaining equipment in working condition with minimal costs,

- extending the service life of equipment.

Result requirements:

Repaired equipment works properly;

Equipment downtime does not exceed the period established by regulations;

The cost of repairs is within the planned funds;

Interested employees are informed about the start of repairs (at least 1 day in advance) and the end of repairs (immediately upon completion).

Performance indicators:

Downtime;

Equipment service life;

Repair and maintenance costs.

2.2. Inputs and outputs of the process, conditions for starting the process

This section describes the start and end conditions for the process. For example:

Entrance: memo from the RP about the start of the tender

Exit: the signed contract was transferred to the accounting department, the tender materials were transferred to the archive.

Term: …

Conditions:

If there are any restrictions or conditions, for example:

Tenders are held for all internal and external work worth over 100,000 rubles. Works worth less than 100,000 rubles are ordered by the RP independently without a tender. The procedure for concluding contracts is described in the regulations “Concluding a contract”.

Or if to start the process, in addition to the main input (start conditions), additional inputs are needed: documents, information, etc.

2.3. Participants in the process

2.2.1. Process owner – (who is responsible for the result and progress of the process, see glossary).

2.2.1. Responsible for process elements:

2.3. Process Procedures

This depicts the sequence and relationship of process procedures, for example:

2.7. Areas of responsibility of participants

It lists which of the participants is responsible for what, for example like this, or in the form of a matrix of distribution of responsibilities:  3. Rules This section includes rules associated with this process.

3. Rules This section includes rules associated with this process.

For example (an example of a piece of rules from the document flow regulations):

Here employees will be able to add new rules that they have agreed on. This should also include information from all orders related to this process.

4.Process procedures

This section is a description of each process procedure in the form: diagram + table of operations + result + requirements for intermediate results. For example:

Next is a description of each procedure in the form of a table: each operation is described by one row of the table.

Next is a description of each procedure in the form of a table: each operation is described by one row of the table.  The regulations also describe documents. They are either described after each procedure (we write requirements for each document that is mentioned in the procedure), or are placed in a separate section.

The regulations also describe documents. They are either described after each procedure (we write requirements for each document that is mentioned in the procedure), or are placed in a separate section.

In addition to the requirements for documents, document forms are included as appendices to the regulations (appendices, forms, forms, etc. are provided by the Customer).

Chapter 4. Documents related to internal accounting

4.1. Internal accounting of a professional participant must be carried out on the basis of an internal document, which is approved by the authorized management body of the professional participant (hereinafter referred to as the Internal Accounting Regulations). Regulations for maintaining internal records may be contained in one or more documents of a professional participant.

The requirements of this chapter do not apply to a professional participant who has entered into an agreement for the provision of internal accounting services with another professional participant. In this case, a professional participant who has entered into an agreement for the provision of internal accounting services must have an internal document establishing the procedure for interaction between the structural units (employees) of such a professional participant when using internal accounting information received from the professional participant providing it with maintenance services. internal accounting.

4.2. The internal accounting regulations should include:

a list of documents on the basis of which internal accounting records are made as provided for in these Regulations, including records on internal accounting accounts (hereinafter referred to as internal accounting documents);

requirements for the content and execution of internal documents used in the internal accounting of a professional participant;

the procedure for organizing document flow and information exchange in order to ensure the implementation of the requirements of these Regulations;

the procedure for opening, maintaining and closing internal accounting accounts;

the procedure and timing for collecting, registering, summarizing and storing internal accounting information, as well as its systematization for reporting to clients based on internal accounting data;

the procedure for assigning and using identifiers (numbers, symbols, codes, abbreviations, indices, code names) in the internal accounting of a professional participant;

the procedure for authenticating employees of a professional participant who have access to the internal accounting information of a professional participant in the mode of reading and (or) changing it, as well as the procedure for accessing this information;

the procedure and timing of reconciliations provided for in Chapter 5 of these Regulations and documenting the fact of their conduct;

the procedure for creating, maintaining and storing a journal(s) for recording orders (demands) of clients provided for in paragraph 7.1 of these Regulations;

the procedure and terms for archiving, backup and storage of internal accounting records of a professional participant, which provide for backup of internal accounting records at least once a working day;

procedure and terms of storage of internal accounting documents;

a list and description of measures taken by a professional participant to ensure the reliability of internal accounting information, as well as to ensure the safety of documents and internal accounting information;

the procedure for operational interaction between divisions and (or) employees of a professional participant that maintain internal accounting, if it is maintained by several divisions and (or) employees of a professional participant, including those geographically remote from each other;

the procedure for determining time for its reflection in internal accounting records, taking into account time zones;

the procedure for grouping and selecting accounting data in accordance with Chapter 8 of these Regulations.

4.3. The internal accounting regulations may also contain other provisions that do not contradict the requirements of the legislation of the Russian Federation and these Regulations.

Each enterprise has local documents regulating its activities. One of the most significant is considered regulations for interaction between departments (sample document will be described below). For the head of an organization, it is an effective management tool. Let's take a closer look at sample regulations for interaction between departments.

Requirements

What should it be regulations? Interaction between the accounting and economic departments services, personnel officers and the calculation and planning department, other structural units of the enterprise inevitably in the process of activity. At the same time, contact between employees should ensure the implementation of assigned tasks in the shortest possible time. Sample regulations for interaction between departments, first of all, must be accessible to performers. If the person responsible for its development writes down all the provisions, but his subordinates cannot understand anything, there will be no meaning in the document. In this regard, when forming, three key principles should be taken into account:

- The document is drawn up based on a business process model. The quality of the regulations will directly depend on the thoroughness of the scheme.

- The document structure is determined by the process model. All points of the scheme must be present in the regulations.

- The information is presented in official, dry language. It is recommended to use short, simple sentences throughout the document. The provisions should be formulated unambiguously. All abbreviations and terms must be deciphered.

Goals

ABOUT sample regulations for interaction between departments provides:

Structure

What are the regulations for interaction between departments? can be considered correctly compiled? Typically the document includes the following sections:

- General provisions.

- Definitions, terms and abbreviations.

- Descriptions of processes.

- Responsibility.

- Control.

Sources of definitions can be legislative acts, GOSTs and other documents. The latter, in particular, include Orders of ministries, departments, and government regulations. In this case, references to regulatory documents, the provisions of which were used, must be included in regulations for interaction between departments. Sample for health care facilities, in particular, contains instructions on the Orders of the Ministry of Health and Social Development, the Ministry of Health of the region.

Application

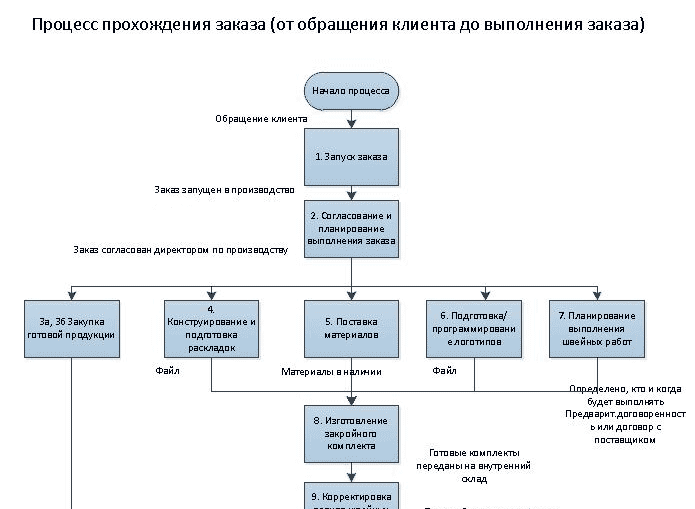

It usually contains a graphical model of the business process. It is depicted as a diagram consisting of several blocks. Graphic images can be created using PC software. Schemes reflect a specific procedure for implementing certain tasks. Visualization is more convenient than text. The diagram clearly shows the beginning of the process and each stage, the connection between them and the final result. This model is often used by developers regulations for interaction between company departments under 223-FZ. The diagram highlights key parameters such as outputs and inputs, participants and clients. If a beginner becomes familiar with such a model, he will immediately understand the specifics of the process and will be ready to implement a certain task.

Instructions

At the first stage, you need to determine the subject of the document and the responsible persons, i.e. who draws up what regulations. Interaction between accounting departments, in particular, is carried out according to a clear scheme established by law. This structural unit always has the most important person responsible for compliance with reporting requirements. He can become the person responsible for drawing up regulations for interaction between departments. Sample The document must be discussed by all employees. For this purpose, a general meeting is organized. If the document regulates a process in which the interests of more than two departments collide, then it is important to involve key employees in the discussion. The person responsible for development should explain to colleagues the importance of implementing the rules.

Description of processes

Its volume will depend on the complexity of the interaction. If the process is simple, and the employee responsible for it understands all the stages of implementation well, then he can himself draw up a scheme for working with other structural units. After this, he should discuss the document with the other participants. If the business process is complex, then each employee develops his own part of the model. After this, all projects are compiled and discussed. During familiarization with the basic document, all interested employees can propose certain adjustments and additions. After this it is transferred to the manager.

Statement

It can be done directly. In this case, the manager himself signs regulations for interaction between company departments. Sample document may also be approved indirectly. In this case, the manager issues an order. The registration data of the administrative act is entered into the approval stamp.

Specifics of the work of the person in charge

Some organizations have a position of quality manager on staff. In practice, certain stages of document preparation have been developed. They must be followed by the manager who composes the main stages:

- Definition of processes.

- Building a diagram.

- Detailed description.

- Composing the text.

The responsible specialist studies the routine of employees in different departments. This is necessary to compile a description of standard situations included in regulations for interaction between departments. Example: “The gas station is inspected using technical means such as... Upon completion of the inspection, a report is drawn up.”

Defining the final goal

The person responsible for drawing up the regulations must have an understanding of all processes, know the responsibilities of employees, and have the appropriate qualifications and level of professionalism. The purpose of the document must be clear to employees. Otherwise, compliance with the regulations will be an additional burden on employees.

Optimization and design

A comprehensive study of the processes occurring at the enterprise allows us to identify weak points. Analysis of situations, results, operations makes it possible to optimize activities. This, in turn, allows us to formulate several scenarios for further development. So, the company can leave everything as is, create a new work model or adjust the old one.

Nuances

It is important that each employee clearly understands what he needs to do and how the results achieved will affect his earnings. That is why it is necessary to discuss the regulations before their approval. The key role is, of course, assigned to the head of the working group (project). The tasks of this specialist include asking pressing questions. He must be able to present a clear model of the process. Each participant sees the picture with his own eyes. It is necessary to achieve a common understanding. Each participant must be explained the responsibility in creating the regulations. In most cases, teams are skeptical about the implementation of such a document. Depending on the complexity of the process, the introduction of regulations takes 4-12 months.

Features of implementation

To introduce a new regulation it is necessary:

- Recognize previous documents as invalid.

- Introduce new local acts to activate the regulations.

- Develop the documents necessary to apply the approved rules.

- Improve or implement new modules of automated information databases.

- Prepare forms for non-unified documents.

- Change or supplement the staffing table.

- Find candidates for new positions, assign or transfer employees.

- Train performers in new rules.

- Conduct explanatory work with employees.

- Carry out a trial implementation of the regulations.

- Correct the text based on the results of experimental execution.

- Put the final version of the document into action.

- Determine procedures for quality control of regulations.

After the measures for implementing the document have been determined, the manager issues an order. It should be noted that due to the duration of the events, the date of approval and direct entry into force of the regulations will differ. Let us next consider the main mistakes that employees make when drawing up a document.

Inconsistency with practice

It is important to entrust the creation of regulations to an employee who is directly related to work activities at the enterprise. Let's say the organization has become very large. Management can easily afford to create a special service whose tasks will include resolving development issues. Accordingly, the department will set the task of describing all processes of the enterprise. But the purpose of this event is not important to them. If the regulations are drawn up by people who are not involved in real activities, then the employee in charge will not implement the scheme. Accordingly, the document does not make sense to work.

Lack of flexibility

Many decision-makers strive for maximum detail. This situation is caused by ignorance of the differences between drawing up regulations and describing real production processes. If the task is to automate operations, their detailing is intended to help employees. The need for regulations arises when many people are involved in production. Their actions are often duplicated, but each person interprets this or that operation in his own way. The regulation is aimed at resolving disagreements. It should be taken into account that employees of the organization must have a certain freedom of action, allowing them to make one or another decision depending on the situation. For example, the client can be answered immediately, and not after some time has passed.

Large volume and complexity of text

A regulation consisting of 5-7 pages is considered optimal. At the same time, its content should be succinct, but brief. It is not recommended to use complex, multi-part sentences. The text must be understandable. In addition, you should pay attention to the terms. You should not replace concepts with synonyms or use abbreviations without decoding.

Interaction between information security and IT departments

Currently, in many enterprises, contacts between these services are very difficult. Difficulties are associated with internal conflicts in the IT and information security departments. There are several options for ensuring their effective cooperation. The first and simplest is the presence of employees (one or more) specializing in information security within the information technology service. Regulations for interaction between IT and information security departments in this case reflects typical approaches to cooperation. The organization of work is carried out on the basis of the established stereotype that information security is part of information technology support. If there are no conflicts between these services in the enterprise, then the manager may think about establishing the information security service as a separate structure of the IT department. Accordingly, it will be necessary to allocate more resources, including financial ones, to support such activities.

Typical sample

The General Provisions specify:

- Purpose of the document. As a rule, there is the following phrase: “These regulations determine the order...”.

- Scope of action. The regulation may apply to workers or facilities.

- Regulatory documents in accordance with which the act was developed.

- Rules for approval, adjustment, cancellation of regulations.

The section "Terms, abbreviations, definitions" contains concepts used in the document. All abbreviations must be deciphered. Terms should be listed in alphabetical order. Each concept is indicated on a new line in units. h. The definition of the term is given without the word “this”, separated by a dash. The section "Description of the process" provides a step-by-step description. It is advisable to introduce subparagraphs. Each of them will correspond to a specific stage. In the same section, employees involved in performing certain operations are indicated. Not only actions are described, but also their results.

Responsibility and control

The regulations must contain an indication of the possibility of applying sanctions to persons who do not comply with the provisions. Liability is permitted within the limits of the law. It can be criminal, administrative or disciplinary. It is mandatory to indicate the full name and position of the employee monitoring the implementation of the regulations.

- Sterlet recipes

- Why does a woman dream about a baby kangaroo?

- Runic inscription to attract customers for your business

- What do the numbers mean in fortune telling on coffee grounds?

- Fortune telling on paper with a ronglis pen

- Orange peels: uses, features and best recipes

- Homemade caramel syrup

- What is a spelling chart for schoolchildren

- How to soak meat in vinegar

- How to bake a meat pie - step-by-step recipes for preparing dough and filling with photos

- Pike cutlets "Original"

- Coconut panna cotta recipe with photo and banana Recipe Vegan panna cotta made from coconut milk

- Banana-nut sponge cake in a slow cooker, photo recipe Chocolate sponge cake with banana in a slow cooker

- Whole chicken baked with garlic and pepper

- Cod liver salads for every taste Cod liver salad with green peas

- Recipes for squash preparations for the winter

- Preparing a milkshake with fresh aromatic strawberries in a blender

- Lunar calendar for December dream book

- Marshmallow recipe with sweetener: what to add to homemade dessert

- Puff pastries with cottage cheese, from ready-made puff pastry