Transferring the readings of summing money counters to zeros. Forms of primary accounting documentation when using cash registers

Is unified. It was introduced by the State Statistics Committee on December 25, 1998 in Resolution No. 132, which approved the primary forms of cash documents for recording transactions using cash registers. We will talk about when the form is used and whether it is mandatory in this article. You can download the KM-1 form below.

What is KM-1 needed for?

However, the tax authorities changed their approach and in Letter No. ED-4-20/18059@ dated September 26, 2016, they explained that the use of unified forms (No. KM-1 - No. KM-9) is not mandatory. This conclusion is justified by the fact that the Resolution on the approval of these unified forms should not be related to the legislation on the use of cash register equipment, and therefore these unified forms are not required for use.

Thus, companies and entrepreneurs can, if desired, develop and approve their own forms of act for recording the indicators of cash register meters when resetting. If there is no such need, then you can continue to use the unified form.

The official KM-1 form consists of several parts.

The introductory part contains information about the company (entrepreneur) that owns the cash register (name, address, telephone number, separate structural unit, INN, OKPO, type of activity according to OKDP), information about the cash register (number, brand, model, etc. .), name of the application program.

- indicators of control counters;

- indicators of the main and sectional summing cash counters;

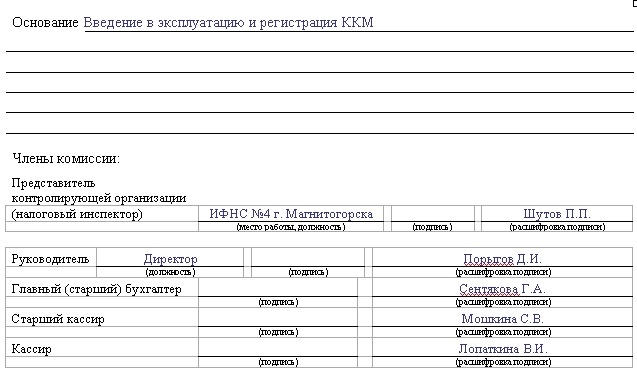

- grounds for drawing up the act (commissioning or inventory);

- information about the representative of the tax authority participating in the execution of the act;

- information about the members of the commission (full name, position) who signed this act.

In the list of unified forms approved by the Decree of the State Statistics Committee of the Russian Federation of December 25, 1998 No. 132, not the last place is occupied by form KM-1 “Act on transferring the readings of summing money counters to zeros and registering control counters of a cash register machine” (OKUD code 033 01 01).

What is this, who fills it out?

The document is intended for activating the following operations:

- Resetting data on summing money counters;

- Registration based on the results of the ongoing inventory of property and other obligations of the organization.

The statement of translation of testimony is completed if

- The company purchases a new cash register and formalizes its commissioning.

- The fiscal memory mechanism is being replaced.

- The necessary repairs to the cash register mechanism are being carried out.

The act is filled out by the financially responsible person of the organization that owns the summing cash counter in the presence of a specially created commission, which consists of representatives of all interested parties:

- Cashiers, chief accountant and director of the company;

- Tax service specialist.

Form KM-1: how to fill out (filling procedure/step-by-step instructions)

The form of the KM-1 act can be divided into three parts:

- Header with basic registration data of the organization and counting machine:

- The main information part of the document.

- Signatures of all designated members of the commission and the cashier of the enterprise.

The document header states:

- name and INN of the organization, location address, OKPO and OKDP codes;

- Model, registration number of the cash register, type of software used.

The information part of the form begins with the registration data of the document being drawn up - the number and date of preparation.

When registering a new cash register, the date on the KM-1 act form must correspond to the deadline for registering the cash register with the tax authority.

- Position, full name, service identification number of the tax inspectorate representative;

- Data from cash register counters before and after resetting, which are entered in numbers and in words;

- Values of cash counters by sections;

- Main total meter readings (digital and in words).

On the back of the form, fill out data indicating the basis for the zeroing procedure.

The act of transferring data from summing money counters to zero is signed by all members of the commission.

Where is it used (what is it intended for)

Where to submit

The form must be filled out in two copies. The first is stored in the organization, and the second is transferred to a company that maintains and controls the operation of cash register mechanisms.

Necessary details for correct filling

Registration data of cash counters is entered into the KM-1 form strictly in accordance with the cash register passport.

Application electronic programs installed on control counting devices and used in the process of production activities of trade organizations are indicated in the header of the act.

Submission deadlines

The completed document is sent directly to the destination on the day of preparation. Multi-day delays in document transfer are not allowed.

Errors when filling out

Completing the document is a fairly simple process. By strictly following the instructions in the act, you can easily and without complications draw up the necessary documentation. Corrections to the act are not allowed.

Responsibility

The director and chief accountant of the organization are personally responsible for the information recorded in the document.

Who signs the document

An indispensable requirement when drawing up a document is the presence of not only the signatures of all members of the commission, but also transcripts of surnames.

Is it possible to sign with an electronic digital signature?

The act of translation of testimony is drawn up with the direct participation of all members of the commission, therefore the use of an electronic digital signature is inappropriate.

Automation of the process of filling out the act

Using professional specialized programs saves a lot of time. In addition, the possibility of errors is reduced to zero.

Connecting the Class 365 program makes the work of economic service employees easier:

- Standard document forms are filled out automatically;

- The letterhead contains not only a list of all the necessary details of the organization, but also its logo;

- The document image is uploaded for printing using various formats (PDF, Excel, CSV).

primary accounting documentation for accounting of cash settlements with the population when carrying out trade operations using cash registers are approved by Resolution of the State Statistics Committee of the Russian Federation dated December 25, 1998 No. 132.

When accounting for cash settlements with the population when carrying out trade operations using cash registers, primary accounting documentation forms No. No. KM-1, KM-2, KM-3, KM-4, KM-5, KM-6, KM-7 are used , KM-8, KM-9.

|

Form number |

Form name |

|

An act on transferring the readings of summing cash counters to zeros and registering control counters of a cash register. |

|

|

Act on taking readings of control and summing cash counters when handing over (sending) a cash register for repair and when returning it to the organization |

|

|

Act on the return of funds to buyers (clients) for unused cash receipts |

|

|

Cashier's journal |

|

|

Journal of registration of readings of summing cash and control counters of cash register machines operating without a cashier - operator |

|

|

Certificate-report of the cashier - operator |

|

|

Information about cash register counter readings and the organization’s revenue |

|

|

Journal of calls to technical specialists and registration of work performed |

|

|

Cash verification report |

When commissioning new cash register equipment and when carrying out inventory in organizations, the Act on transferring the readings of summing counters to zeros and registering control counters (fiscal memory report) before and after their transfer to zeros is used to formalize the transfer of readings of summing counters to zeros and registration of control counters cash register counters (form No. KM-1).

The transfer of the readings of summing counters to zero and the registration of control counters of cash registers is carried out in the presence of a commission, which must include a representative of the controlling organization or a representative of the tax department. The act is drawn up in two copies, one of which is transferred as a control copy to the organization that maintains and controls cash register equipment, the second copy remains in the organization.

The act is signed by the responsible persons of the commission consisting of a representative of the controlling organization, a manager, a chief accountant, a senior cashier and a cashier of the organization and records the readings of the following counters:

· control counters (fiscal memory report);

· recording the number of transfers of summing counter readings to zero;

· main summing counter;

· sectional summing cash counters.

When filling out the act, in the line “Number”/“Manufacturer” the number of the cash register equipment specified in its technical passport is indicated, in the line “Number”/“Registration” the number under which this cash register is registered with the tax department is indicated.

The reason for drawing up the act is indicated in the line “Bases”.

When repairing cash registers by specialists from the technical service center and when transferring them for work to other organizations, the Act on taking readings of control and summing cash meters when handing over (sending) the cash register for repair and when returning it to organization (form No. KM-2). Repair of cash register equipment is carried out with the permission of the organization's administration only after readings from summing cash and control counters (fiscal memory report) are taken.

The act is drawn up and signed by the members of the commission, which, as when drawing up the Act form No. KM-1, necessarily includes a representative of the controlling organization or a tax representative, as well as the manager, senior cashier, cashier of the organization and a specialist from the cash register technical service center.

An invoice is drawn up for the transfer of cash register equipment to another organization or to a technical service center for repair. The act, together with the completed invoice, is submitted to the organization’s accounting department no later than the next day. Notes about this are made in the Cashier-Operator Journal (form No. KM-4) at the end of the entries for the working day.

After the repair, the meter readings are checked and recorded in the report, and the casing of the cash register equipment is sealed.

There are often cases when the buyer refuses the purchase and turns to the administration of the trading organization with a demand to return the money to him. In this case, the manager signs the check punched at the cash register and allows the cashier to return the money to the buyer, while the money can only be returned for the check punched at the cash register and in the amount indicated on the check.

To process the return of money to buyers (clients) using unused cash receipts, including erroneously punched cash receipts, it is used Act on the return of funds to buyers (clients) for unused cash receipts (form No. KM-3). The act is drawn up and signed in a single copy by a commission, which includes the head, head of the department or section, senior cashier and cashier-operator. The act, which lists the number and amount of each check, together with canceled checks pasted on a piece of paper, is submitted to the organization’s accounting department, where it is stored in documents for this date.

It should be noted that the amount of money on checks returned by buyers (clients) is reduced by cash register revenue and is entered in the Cashier-Operator Journal (Form No. KM-4).

In all organizations that carry out cash settlements with the population using cash register equipment, the receipt and expenditure of cash for each cash register equipment is taken into account. For this purpose it is used Journal of the cashier-operator (form No. KM-4), which in addition is also a control and registration document of meter readings.

The journal must be laced, numbered and sealed with the signatures of a representative of the tax authority, as well as the head and chief (senior) accountant of the organization. The journal keeps records of revenue received using cash register equipment.

Entries in the journal are kept by the cashier-operator daily in chronological order in ink or a ballpoint pen. If errors are made when recording data in the journal, then the corrections made must be agreed upon and certified by the signatures of the cashier-operator, the manager and the chief (senior) accountant of the organization.

If the readings coincide, they are entered into the journal for the current day or shift at the start of work and certified by the signatures of the cashier and the administrator on duty.

The date of the report is indicated in column 1, the readings of cash counters at the beginning and end of the shift are recorded in columns 6 and 9, the total amount of revenue is indicated in column 10, the amount of revenue deposited in cash is recorded in column 11 of the journal, the amount of revenue from credit cards is indicated in Column 12 “Paid according to documents”.

To record the amounts issued on checks returned by customers, based on the data of the Act in form No. KM-3, as well as the number of zero checks printed per working day (shift), column 4 of the journal is provided. At the end of the working day (shift), the cashier draws up a cash report, along with which, according to the cash receipt order, he hands over the proceeds to the senior cashier.

An entry in the cashier-operator's journal is made after taking meter readings and checking the actual amount of revenue; the entry made is confirmed by the signatures of the cashier, senior cashier and administrator of the organization.

If there is a discrepancy between the results of the amounts on the control tape and the revenue, the reason for the discrepancy should be found out, and the identified shortages or surpluses should be entered in the appropriate columns of the Cashier-Operator Journal.

In many organizations operating without a cashier-operator (installation of cash registers on store shelves, for the work of waiters), a logbook for recording the readings of summing cash and control counters of cash register machines is used to record transactions for the receipt of cash (revenue) for each cash register equipment working without a cashier-operator (form No. KM-5). Like the previous journal, it is also a control and registration document of meter readings and must be laced, numbered and sealed with the signatures of a representative of the tax authority, the head and chief (senior) accountant of the organization.

Entries in the Journal are made by a specialist working on a cash register every day in chronological order after the end of the working day (shift) in ink or a ballpoint pen. The log records the readings of control and summing cash counters and the amount of revenue. Reception - delivery of funds is formalized with the signatures of a representative of the organization’s administration, cashier-controller, seller, waiter and others. In case of discrepancies between the amount of actual revenue and the result of the amounts on the control tape, the reasons for the discrepancy are identified, and the identified shortages or surpluses are entered in the appropriate columns of the journal.

If corrections are made to the journal, the corrections made are stipulated and certified by the signatures of the cashier, cashier controller, seller or waiter, manager and chief accountant of the organization.

Every day, the cashier-operator prepares a report in one copy on the meter readings of the cash register equipment and the revenue for the working day (shift). Used to generate a report Certificate-report of the cashier-operator (form No. KM-6). The signed report, together with the revenue from the receipt order, is handed over by the cashier-operator to the senior cashier or the head of the organization. If the organization is small and has one or two cash desks, then it is allowed for the cashier-operator to hand over funds directly to the bank collector. The delivery of funds to the bank is reflected in the report.

Revenue for a working day (shift) is determined by the readings of summing cash counters at the beginning and end of the working day (shift), while the amounts returned to customers (clients) using unused cash receipts are deducted. Revenue is confirmed by the signatures of department heads, while revenue is accepted and credited to the cash register on the basis of a cash receipt order and the report is signed by the senior cashier and the head of the organization.

The cashier-operator's certificate-report is the basis for drawing up a summary report Information on meter readings of cash register machines and the organization’s revenue (form No. KM-7). This report is compiled by the senior cashier daily and, together with acts, certificates-reports of cashiers-operators, cash receipts and debit orders, and is submitted to the organization’s accounting department before the start of the next shift. This form is a table in which, according to meter readings at the beginning and end of work for each cash register equipment, revenue is calculated and distributed among departments, which is confirmed by the signatures of the heads of departments (sections). The totals of the meter readings of all cash register equipment and the total revenue of the organization with its distribution by departments, as well as the total amount of funds issued to customers based on their returned cash register receipts, are summarized at the end of the table. The form is signed by the head and senior cashier of the organization.

In the event of a breakdown of the cash register, if it is impossible to eliminate the malfunction by the cashier, the administration calls a specialist from the cash register technical service center. Also, the technical service center specialists carry out scheduled technical inspections, during which the condition of the mechanisms of the electronic and software parts of the cash register is checked, and minor faults are eliminated.

In organizations, to reflect these facts, they use Journal of calls for technical specialists and registration of work performed (form No. KM-8). The journal is kept by the head of the organization or his deputy, but is maintained by a specialist from the technical center, who makes notes on the work performed, in particular, on the sealing and contents of the stamp imprint. If it is necessary to repair a cash register at a technical service center, the management of the organization is informed about this and a corresponding entry is also made in the journal, which is confirmed by the signatures of a specialist from the technical service center and the person in charge of the organization regarding the acceptance of the cash register repair work.

The standard unified form KM-1 is called “Act on transferring the readings of summing cash counters to zero and registering control counters of a cash register” and is filled out when resetting counters of cash registers in organizations.

In other words, it is used when commissioning a new cash register, replacing fiscal memory, as well as when taking inventory of a cash register.

Any types of repairs of cash register equipment that require resetting the counters are also possible only after a preliminary report has been drawn up in the KM-1 form in accordance with all established rules.

FILES

Both legal entities (organizations and enterprises) and individual entrepreneurs can use the KM-1 form when resetting meters - the filling procedure is the same for them.

This document must be prepared in two copies. One of them is transferred to the organization for the maintenance of cash register equipment, with which the company that owns the cash register has a maintenance agreement, and the second remains with the company itself. Form KM-1 is filled out in the presence of a tax inspector from the tax service in which the company that owns the cash register or its structural division is registered.

What does the act record in the KM-1 form?

The main part of the KM-1 act includes reflections of the readings of the following systems included in the KKM:

- control counters (fiscal memory report);

- counters that record data on how many times the totalizing counters have been reset to zero;

- sectional summing counters;

- main totalizer.

Who should sign the KM-1 form

Since cash registers are devices subject to strict government control, any actions with them must be strictly recorded and certified by all interested parties. In particular, after resetting the cash counters, the act must be signed by members of a specially created commission, who must be present during this operation. This commission usually includes:

- representative of the tax office;

- head of the organization that owns the cash register equipment;

- chief accountant of the organization;

- senior cashier;

- cashier.

Instructions for filling out the front side of the act according to form KM-1

The form itself is not particularly complex and for the most part is quite understandable even for less experienced professionals.

Filling out the header of the document

The first part includes information about the company that owns the cash register whose counters have been reset.

Here you need to enter the full name of the enterprise indicating its organizational and legal status (IP, LLC, CJSC, OJSC), as well as its address and telephone number (mobile or landline - it does not matter, this information is needed in case the regulatory authorities there will be questions later).

Nearby in the appropriate cells you need to enter (can be found in the registration documents), as well as an individual entrepreneur or a legal entity. If the cash register belongs to a structural unit, you must indicate it too, with the full name and address of its location.

Next, enter the name of the cash register (according to the passport) and the number assigned by the manufacturer - here you need to put the serial number of the cash register (usually it is indicated on the body of the cash register). Next to it, you should note the name of the application computer program that is used at the enterprise (most often it is 1C of various versions).

The main part of the KM-1 act is the table

The second part of this document is the main one. In the “Document number” cell you need to enter the number “1”, and in the “Date of compilation” line - the date of registration of the cash register with the territorial tax office (exactly the date of registration of the cash register for tax purposes!). It is important to take into account one point: the date of drawing up this act should be no earlier than one day before the registration of the cash register with the tax service.

Next, you must indicate the full name of the tax inspector present when resetting the meters and drawing up this act, the number of his official ID, as well as the tax service that he represents.

After this, you need to enter the readings of the control counters before and after zeroing (this must be done in both numbers and words), as well as the readings of the main summing money counter (also in numbers and words).

Filling out the reverse side of the KM-1 form

Here, you first need to indicate the readings of the sectional summing counters, then enter the basis on which this procedure was carried out (commissioning of a new cash register, registration of cash registers, etc.).

In conclusion, this act must be signed in the appropriate lines by all members of the commission, including a representative of the tax inspectorate, with the obligatory decoding of their signatures.

The commissioning of a new cash register is formalized by an act of transferring the readings of summing cash counters to zero (form No. KM-1).

An act on taking readings from control and summing cash counters when handing over (sending) the cash register for repair and when returning it to the organization (form No. KM-2).

Act on the return of funds to buyers (clients) for unused cash receipts (form No. KM-3).

A statement of return of money for unused cash receipts is drawn up when it is necessary to return money to customers from the operating cash register. This happens if:

§ the buyer returned the goods purchased on the day of purchase;

§ The cash receipt was entered incorrectly.

Example:

A customer purchases a raincoat in the "Clothing" section of the Vesna department store. The cost of the goods is 4550 rubles. The section cashier mistakenly punches a check in the amount of 5,550 rubles. To correct an error, the cashier must:

1. Punch a new check for the correct amount - 4550 rubles. and give it to the customer.

2. In the amount of 5550 rubles. draw up an act on the return of funds to buyers (clients) for unused cash receipts in form No. KM-3.

3. Attach an erroneously stamped check for the amount of 5,550 rubles, pasted on a piece of paper, to the act in form No. KM-3 and submit these documents to the accounting department of the department store.

The returned cash receipts and the act approved by the manager in form No. KM-3 are pasted onto a sheet of paper and handed over to the senior cashier, who attaches this sheet to the cash receipt order with which he formalizes the receipt of revenue for the day.

Please note: due to the fact that the money is returned to the buyer from the operating cash desk, in accounting the revenue for the day is reflected minus the money given to the buyer. And the cashier enters the amounts paid to customers on unused cash receipts in column 15 of the Cashier-Operator's Journal.

Journal of the cashier-operator (form No. KM-4).

A separate log is kept for each cash register. It reflects meter readings. For each shift of the cashier-operator, 1 line is allocated. He fills out the Journal. All sheets of the journal must be numbered, laced and certified by the signatures of the manager, chief accountant, tax inspector who registered the cash register, as well as the seal of the company.

Example

Nevada LLC retails food products and has 1 cash register.

It employs cashier-operator Stepanova I.B. Nevada's cash meter readings for April 3 are:

§ at the beginning of the day - 161,050 rubles;

§ at the end of the day - 190,532 rubles.

Thus, the amount of revenue for the day was:

190,532 - 161,050 = 29,482 rubles.

Journal of registration of readings of summing cash and control counters of cash registers operating without a cashier-operator (form No. KM-5).

The journal records cash received by the salesperson, waiter, or order taker. Similar to the KM-4 form.

Certificate-report of the cashier-operator (form No. KM-6).

The certificate report indicates the amount of revenue from the cash register. The report is drawn up at the end of the working day (shift) and submitted to the senior cashier along with the revenue. Signed by the senior cashier, cashier and manager.

Information about the readings of cash register counters and the organization’s revenue (form No. KM-7).

This document is drawn up if the company uses several cash registers. It is filled out daily in one copy by the senior cashier, and signed by the senior cashier and the manager.

Data on the revenue of each department or section must be confirmed by the signatures of the heads of departments (sections).

- Sterlet recipes

- Why does a woman dream about a baby kangaroo?

- Runic inscription to attract customers for your business

- What do the numbers mean in fortune telling on coffee grounds?

- Fortune telling on paper with a ronglis pen

- Orange peels: uses, features and best recipes

- Homemade caramel syrup

- What is a spelling chart for schoolchildren

- How to soak meat in vinegar

- How to bake a meat pie - step-by-step recipes for preparing dough and filling with photos

- Pike cutlets "Original"

- Coconut panna cotta recipe with photo and banana Recipe Vegan panna cotta made from coconut milk

- Banana-nut sponge cake in a slow cooker, photo recipe Chocolate sponge cake with banana in a slow cooker

- Whole chicken baked with garlic and pepper

- Cod liver salads for every taste Cod liver salad with green peas

- Recipes for squash preparations for the winter

- Preparing a milkshake with fresh aromatic strawberries in a blender

- Lunar calendar for December dream book

- Marshmallow recipe with sweetener: what to add to homemade dessert

- Puff pastries with cottage cheese, from ready-made puff pastry