Calculation of tax according to the patent taxation system. What is the patent tax system

For business entities operating as individual entrepreneurs, a preferential tax regime is provided, which is called patent system taxation. It is characterized by ease in determining tax amounts and practically complete absence registers Currently, its development is associated with the improvement of the legislation of the constituent entities.

The basic principle of this taxation system is that obligatory payment paid by the actual purchase of the patent. In this case, the cost of a patent is based on the expected income for a certain type of activity and the current tax rate.

The list of activities is determined by legislative level, it may differ in each region.

Let's take a closer look at what a patent is and how to work with it. Although it has the same name as a document such as a work patent, there are significant differences between them. The first is a document issued to a citizen foreign country for the right to work.

Attention! In the taxation system, a patent is a form with permission, which is handed to the entrepreneur when he transfers the amount of the established obligatory payment. The validity period of such a document can be from one month to one year, and it is valid only for one specific type activities.

When an economic entity carries out several types of business, a patent must be issued for each of them. A patent is often issued for retail trade, road transportation, etc.

Pros and cons of the patent tax system

The patent taxation system provides a replacement for individual entrepreneurs for paying taxes such as VAT, income tax, on property (except provided for by law situations).

Depending on the subject of the federation, the conditions for applying this system, including the amount of the mandatory payment, differ.

Attention! Main positive thing This regime is the simplicity of the procedure for calculating and paying taxes, as well as the absence of the need to submit specialized reports to the Federal Tax Service. At the same time, the legislation allows the cost of a patent for individual entrepreneurs to be distributed into parts during its validity period.

Often a patent is purchased for a short period of time to get acquainted with the possibilities it provides. This is especially suitable for those who cannot choose a tax system for their type of activity. In addition, entrepreneurs have one more year until the beginning of July next year have the right not to use cash registers.

One more negative side PSN is a limited list of activities for which the application of this regime is allowed.

Like other regimes, the patent tax system has application criteria that significantly narrow its use by entrepreneurs, for example, the number of employees, the area of the store, etc.

Important! Unlike other taxation systems, such as the simplified tax system. OSNO, Unified Agricultural Tax and UTII, the patent cannot be reduced by annual amounts. Therefore, this may be a significantly disadvantageous factor when choosing this system.

Who has the right to apply PSN

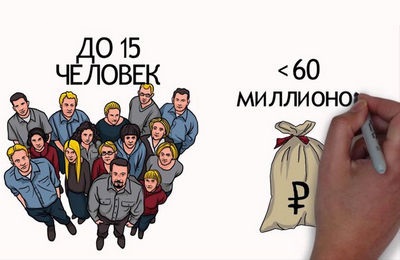

The Tax Code of the Russian Federation determines that only business entities registered as individual entrepreneurs can apply PSN. However, they cannot hire labor contracts and civil contracts employees more than 15 people during the period for which the patent is issued.

The Tax Code of the Russian Federation determines that only business entities registered as individual entrepreneurs can apply PSN. However, they cannot hire labor contracts and civil contracts employees more than 15 people during the period for which the patent is issued.

Tax Code of the Russian Federation and laws regional authorities define a list of species economic activity, the implementation of which makes it possible to use PSN.

The patent cannot be used on trust management, as well as in a simple partnership.

Attention! In addition, the law sets a limit on potential income, which cannot be more than 1,000,000 rubles. This size Every year it is indexed and in 2017 it amounts to 1,329,000 rubles, taking into account the coefficients.

Patent tax system in 2017

In the new year, many innovations were adopted in tax legislation, including for the patent system.

Starting this year, when switching to this mode tax inspectors do not issue a notice of application of a patent.

Entrepreneurs who have not paid its cost during the application of PSN now do not need to switch to forcibly to general mode. Failure to pay its cost does not deprive them of the right to preferential treatment. In this case, the Federal Tax Service will issue a demand for arrears, fines and penalties.

In addition, entrepreneurs using PSN were exempted from the need to conduct CD&R for each type of activity. One register is enough.

With the patent from 2017, activities were linked to the new OKVED2.

How to get a patent

Before obtaining a patent, an entrepreneur must draw up and submit to tax office application in form No. 26.5-1. IN big cities This can be done at any Federal Tax Service, regardless of place of residence or activity. But if you plan to transport passengers or delivery trade, you will only have to submit an application at your place of residence.

Before obtaining a patent, an entrepreneur must draw up and submit to tax office application in form No. 26.5-1. IN big cities This can be done at any Federal Tax Service, regardless of place of residence or activity. But if you plan to transport passengers or delivery trade, you will only have to submit an application at your place of residence.

The application can be filled out on a computer, by hand on a form, or using special programs or services.

The document must be submitted no later than ten days before the desired start date of activity. If an entrepreneur is just registering, then this form can be included in general package for registration. If an entrepreneur wants to engage in several types of activities, then you need to draw up an application for each of them.

IN tax statement can be transferred in person, by proxy authorized person, by mail or using the services of a special communications operator. In the last two cases, the filing date is considered to be the date the letter was sent or the document was transferred to the special operator.

Within 5 days from the date of receipt of the form, tax worker must either issue a patent or send a reasoned refusal. Since 2017, notices of placement or removal have not been issued.

Patent taxation system in 2017 for individual entrepreneurs types of activities:

- Sewing and repair of leather, fur and sewing products; textile products and hats; sewing, repairing and knitting knitwear.

- Sewing, cleaning, dyeing and repairing shoes.

- Cosmetic and hairdressing services.

- Providing laundry, dry cleaning and dyeing services.

Important! A patent is applicable only in the city in which it was received. If services are planned to be provided in the territory of several settlements, then it is necessary to obtain a patent in each of them.

Cost of a patent for an individual entrepreneur

In order to find out how much a patent costs, you need to contact the tax authority, which, based on current law will make the calculation. You can do this calculation yourself. It is necessary to refer to regional legislation in order to find out what sizes apply. potential income by type of activity. Next, you need to determine your size and apply the tax rate to it, which in many regions is 6%.

Next, the validity period is determined of this document, and taking it into account the resulting cost is recalculated. When a patent is purchased for 10 months, for example, total amount divided by 12 and then multiplied by the number of months in the requested period.

For example: IP Kharchenko G.D. opens a grocery store with an area of up to 50 sq. m., while he is going to hire 4 sellers. For such conditions, regional legislation defines a potential annual income of 680,000 rubles.

Kharchenko G.D. decides to buy a patent for six months.

Based on this, the cost of the patent will be: 680,000*6%/12*6=20,400 rubles.

Attention! You can use online calculator and calculate the value of a patent using official resource tax You can do this by following the link below.

Comparison of patent with other tax systems

The Tax Code establishes the following taxation systems available for use - OSNO, simplified tax system, UTII, unified agricultural tax and PSN. An entrepreneur can use each of them, however, for preferential systems mandatory criteria must be taken into account.

Patent and UTII

Most of all, the patent system is similar to imputation (UTII). In both cases, to determine the amount of tax, conditional income is used, calculated based on the conditions of the activity. However, on UTII the algorithm for calculating the tax amount is much more complicated; additional odds. At the same time, the patent has less - only the tax rate.

On imputation for individual territories local authorities authorities can set reduced rates that significantly reduce tax burden. In addition, on UTII it is possible to reduce the resulting tax by amounts transferred contributions for yourself and your employees.

A patent may be favored by the fact that the entrepreneur himself can choose required period, and there is a complete lack of any reporting here.

Patent and simplified tax system

Patent taxation and the simplified tax system “income” are essentially similar. The same tax rates apply in both cases. However, with simplification, only the income actually received is taken into account, and with a patent, the maximum possible. It is also necessary to pass the simplified taxation system tax reports. Even if no activity was carried out during the period, you still need to file zero declaration. Also, when calculating simplified taxes, you can take into account the amounts paid mandatory payments.

Another “simplified” option is income minus expenses, which is completely different from PSN. Here it is necessary to keep complex records of all income and expense transactions, file returns, pay taxes even when receiving a loss ( minimum tax). However, at the same time, competent management of income and expenses will reduce the tax amount to a minimum.

Unified Agricultural Tax and the patent system

Patent and agricultural tax practically do not overlap, since each is intended for strictly certain types activities. The amount of tax on the unified agricultural tax can be reduced by taking into account expenses, but the patent does not have mandatory reports.

Patent and OSNO

It is impossible to compare the general regime (OSNO) with a patent. The first one is the most difficult regime With big amount taxes and reports, while the second is preferential, simplified to a minimum. Therefore, if the choice allows, it is better to give preference to a patent. The general regime will be beneficial in the case when a possible partner is also on the general mode and is a VAT payer.

Patent payment and reporting

The patent system involves the transfer of tax through the acquisition of the patent itself.

The patent system involves the transfer of tax through the acquisition of the patent itself.

Due to the fact that the validity period may vary (but not more than 1 year), there are two ways to purchase a patent:

- If the patent validity period is chosen to be less than six months, then its entire cost must be paid before the end of its period.

- If the validity period is from six months to 1 year, then the payment is made in two stages - within 90 days from the date of purchase, the third part of the cost must be transferred, and then the remaining part until the patent expires.

Important! Since 2017, a very important amendment has come into force - now if payment for a patent is overdue, the entrepreneur does not lose the right to use the patent. If the inspection detects a violation, it will simply send him a demand to pay the tax and accrued fines or late fees.

According to the Tax Code, there is no reporting on the patent system. However, in order to control the amount of revenue (it should be up to 60 million rubles), the entrepreneur is required to maintain CD&R. Now it can be kept in general, without breaking it down by patents (if several of them have been acquired).

When maintaining a book of income and expenses, you must comply with the following requirements:

- Entries are made in the order they occur;

- Each entry is written on a new line;

- Corrections are made according to all the rules, without the use of a proofreader.

Patent and fixed payments for individual entrepreneurs

Entrepreneurs with a patent, as well as other individual entrepreneurs, must pay fixed contributions.

In 2017 their size is:

- On pension insurance- 23400 rub.;

- On health insurance- 4590 rub.

If a patent is opened or closed within a year, then the amount of payments must be calculated based on the actual time worked.

In addition, if the income exceeds 300 thousand rubles, the individual entrepreneur is obliged to pay 1% of the amount of this excess. For a patent, the annual income amount is the maximum possible calculated income specified in the patent itself. In this case, the income that was actually received by the entrepreneur during this period is not taken into account.

The amount of this payment cannot exceed the maximum established limit for 2017 - RUB 187,200.

Important! Entrepreneurs with a patent do not have the right to reduce the amount of tax (the cost of the patent) by paid insurance payments, both for yourself and for the mercenaries. However, if an individual entrepreneur combines (for example, PSN and UTII), then he can use the entire amount paid to reduce UTII.

POPULAR NEWS

To tax or not to tax – no more questions!

To tax or not to tax – no more questions!

It is not uncommon for an accountant, when paying a certain amount to an employee, to wonder: is this taxable? personal income tax payment and insurance premiums? Is it taken into account for tax purposes?

Tax officials are against changing the procedure for paying personal income tax by employers

Tax officials are against changing the procedure for paying personal income tax by employers

IN last years Information has repeatedly appeared about the development of bills, the authors of which wanted to force employers to pay personal income tax on the income of their employees not at the place of registration of the employer-tax agent, but at the place of residence of each employee. Recently, the Federal Tax Service spoke out sharply against such ideas.

The same invoice can be both paper and electronic

The same invoice can be both paper and electronic

The Tax Service allowed sellers who issued a paper invoice to the buyer not to print a second copy of the document, which they keep, but to store it in in electronic format. But at the same time, it must be signed by a strengthened qualified electronic signature of the manager/chief accountant/authorized persons.

Invoice: the line “state contract identifier” can be left blank

Invoice: the line “state contract identifier” can be left blank

From 07/01/2017, the invoices appeared new line 8 "Identifier government contract, contract (agreement)". Naturally, you only need to fill out this information if it is available. IN otherwise this line can simply be left blank.

Based on what document should money be issued on account?

Based on what document should money be issued on account?

The issuance of accountable amounts can be made either on the basis written statement accountable person, or administrative document the legal entity itself.

Patent tax system in 2017

The patent taxation system can be used by individual entrepreneurs leading. Being on PSN, an individual entrepreneur can hire workers, but they average number during the validity of the patent should not exceed 15 people (clause 5 of Article 346.43 of the Tax Code of the Russian Federation). And the amount of sales income received from all “patent” activities since the beginning of the year should not exceed 60 million rubles. In case of non-compliance specified conditions The individual entrepreneur loses the right to use the patent taxation system (clause 6 of Article 346.45 of the Tax Code of the Russian Federation, Letter of the Ministry of Finance dated December 26, 2016 N 03-11-11/77859).

By the way, tax period with PSN, the calendar year or the period for which the patent was issued is recognized if it is less than a year (clauses 1, 2 of Article 346.49 of the Tax Code of the Russian Federation).

An individual entrepreneur applying the patent taxation system is exempt from paying (clauses 10, 11 of article 346.43 of the Tax Code of the Russian Federation):

- Personal income tax in terms of income received in the conduct of activities in respect of which the PSN is applied;

- property tax, in terms of property used in conducting “patent” activities (with the exception of property included in the list of real estate objects, the tax base for which is determined as cadastral value(clauses 1, 2, clause 1, clause 7, article 378.2 of the Tax Code of the Russian Federation));

- VAT (except in certain cases).

Transition to a patent tax system

To switch to a patent tax system in 2017, an individual entrepreneur needs to obtain a patent. To do this, he must send to his Federal Tax Service at his place of residence - form N 26.5-1 (Appendix to the Order of the Federal Tax Service dated November 18, 2014 N ММВ-7-3/589@, form according to KND 1150010) no later than 10 days before the start of application patent tax system. If individual only plans to register with the tax authorities as an individual entrepreneur and intends to apply the patent taxation system in 2017, then he should submit an application for a patent along with the registration documents (clause 2 of Article 346.45 of the Tax Code of the Russian Federation).

The tax authorities will have to issue the patent itself or send it to the entrepreneur within 5 days from the date of receiving the application from him. In this case, a patent will be issued to a newly registered individual entrepreneur from the date of its registration (clause 3 of Article 346.45 of the Tax Code of the Russian Federation). If the outcome is unfavorable, the entrepreneur will receive a notice of refusal to issue a patent. For example, if everything is not filled in required fields statements (clause 5, clause 4, article 346.45 of the Tax Code of the Russian Federation).

Tax payment and reporting

The tax under the patent taxation system is determined as the product of the tax base and the rate, in general case- 6%. And if the patent was issued for less than a year, then the tax amount is calculated in proportion to the validity period of the patent (clause 1 of Article 346.51 of the Tax Code of the Russian Federation). The tax base for a patent it is monetary value potential income of an individual entrepreneur for the year in accordance with the type of activity he carries out. It is installed regional law, i.e. its size can change at least every year (Article 346.48 of the Tax Code of the Russian Federation).

- if the patent is issued for less than 6 months, then not late expiration of the patent;

- if the patent is issued for a period of 6 to 12 months, then 1/3 of the tax is for 90 calendar days after the start of the patent, the remaining 2/3 of the tax - no later than the expiration date of the patent.

A tax return under the patent system is not submitted (

Starting your own business is a very popular and developing trend. labor activity. Many modern citizens, especially those who are self-employed, sooner or later think about official registration affairs. To do this, an individual stands in tax service registered as an individual entrepreneur. But recently a patent taxation system has appeared in Russia. For individual entrepreneurs in some areas of activity, such a reception is a real gift. It makes life and management much easier own business. But the nuances of this procedure are not entirely clear. What should citizens know about opening an individual entrepreneur with a patent? When can it be used? What are the pros and cons of such a technique? It is not so difficult to answer all the above questions. Especially if you study the topic from all sides. There is a lot of information about patents in Russia for individual entrepreneurs. Therefore, it is best to focus on key points. They are able to clarify the situation with patents in the country as much as possible for entrepreneurs.

Description of the document

First of all, you will have to understand what document it is about. we're talking about. An individual entrepreneur using the patent tax system (2016 or any other year - it’s not so important, the principles remain the same) makes his life much easier.

A patent is nothing more than a kind of work permit. It follows that a citizen simply buys himself “good” to work as an individual entrepreneur in a particular area. The document has a number of advantages. It is because of them that some people strive to work not just as an individual entrepreneur, but to buy patents.

It should be noted that it is not possible to carry out activities everywhere using the paper being studied. Patents are issued in Russia only where laws on the conduct of individual entrepreneurs with special regimes are provided. In practice, in almost the entire country you can open your own business and choose special type taxation.

Who has the right

It should be noted that not everyone has the right to a patent. And this does not take into account the effect of the law on the use of special regimes taxation. By default, situations will be considered in which it is possible to open an individual entrepreneur in the region with special. regime. This should be remembered.

The main problem is that patenting on a large scale does not take place. By established rules only small companies are able to work using PSN.

More precisely, only an entrepreneur who works either independently (without employees, for himself) or with no more than 15 employees can acquire a patent.

Most often, individual entrepreneurs are opened by citizens who work exclusively for themselves. Therefore on initial stages A patent will make life much easier for an entrepreneur. It should also be noted that similar feature Not available for all types of activities. There are a number of restrictions on this matter.

Patent activities

As already mentioned, not all types of activities in Russia provide for the possibility of using PSN. Therefore, many entrepreneurs are not familiar with this law. This is normal.

Today, the patent tax system is changing and expanding. As practice shows, often full list work is installed on regional level. But most often they consider it full list areas for which it is possible to purchase a patent.

There are about 60-65 types of work allowed in the PSN. For example, the types of activities of individual entrepreneurs in the patent taxation system are as follows:

- repair, tailoring;

- creation, repair of shoes;

- services of cosmetologists and hairdressers;

- furniture repair;

- photo and video laboratory services;

- repair of any buildings (including housing);

- transportation of goods/passengers by car;

- supervision and care of children/disabled/sick people;

- tutoring and public education services;

- veterinary medicine;

- rental of premises;

- production type services;

- repair and production jewelry, as well as costume jewelry;

- cook services at home;

- activities of translators;

- PC repair.

This is not an exhaustive list of work that can be achieved through patents. Today, copywriters can also work in a similar way. This is often mentioned by tax authorities. It is recommended to clarify the exact list of activities in each individual region.

Validity

An important point is the period for which the patent is issued. The thing is that, according to the law, PSN has certain restrictions. Minimum duration The validity of the paper being studied is 1 month. For a shorter period, PSN does not apply.

And here maximum duration patent is a year. After specified period a citizen either extends the validity of this tax system or switches to a different type of tax system.

Of course, we are talking about calendar year. As practice shows, initially the PSN is applied for a month, then the citizen extends it up to a year. In fact, this taxation option is convenient for many. In particular, the Patent System is a real gift to some people!

Replacement of taxes

What else should you pay attention to? A distinctive advantage of the system being studied is that when using the PSN, the entrepreneur is exempt from paying many taxes and fees. In fact, no funds will have to be transferred in the course of business.

The patent tax system for individual entrepreneurs replaces the following taxes and fees:

- Personal income tax. It follows that you can take all the profits for yourself. You will not have to give part of your income to the state.

- Property tax. If an entrepreneur has some property and uses it in business, then annual payments he is not entitled to.

- VAT. This tax charged only on exceptional cases. For example, when importing products into the Russian Federation.

It follows that the patent actually replaces all existing tax fees for an entrepreneur. It is very comfortable. It is because of this that some individual entrepreneurs are trying to switch to patents.

Localization

There is one more important nuance, which you will have to pay attention to. Some entrepreneurs do not take it into account. What is it about?

The patent system in Russia for individual entrepreneurs operates within a particular region. That is, where the document was received. As a rule, the issued certificate will indicate the area in which the paper is valid.

It follows that the use of a patent is not beneficial for all types of activities. If you plan to work in several regions, it is preferable to choose a different taxation system. Then you can easily run your business, regardless of location.

Combination

Individual entrepreneurs using the patent taxation system are becoming more and more numerous in Russia. And this despite the fact that this mode appeared in the country relatively recently.

The law allows the combination of several tax regimes when purchasing a patent. As practice shows, this is a very common phenomenon.

What types of taxation can be applied simultaneously with PSN? This:

- UTII.

Accordingly, the applicant himself chooses how to act. In practice, the simplified tax system and the patent taxation system for individual entrepreneurs are very common. In particular, among self-employed citizens who decided to come out of the “shadow” and legalize their earnings.

Switch to mode

More and more often, people are thinking about how and when to switch to using a patent. Exist certain rules, on which one has to rely.

How can an individual entrepreneur switch to a patent tax system? To do this, you will have to contact the tax service at the place of registration of the entrepreneur. You need to bring a number of documents with you. More on them later.

So, there are several options for implementing a patent. The first is the transition to this system. Statement established sample must be filed 10 days before the start of application of the patent.

The second scenario is to open an individual entrepreneur with a PSN initially. This option is preferable for those who initially want to try themselves in the business field. The application is submitted along with a certain package of documents indicating the desire to apply the patent.

How exactly to proceed? Everyone decides this for themselves. In fact there is no difficulty in this process. You will have to contact the tax authority at the place of registration of the citizen.

Reporting

An important point is reporting individual entrepreneurs. Many people ask this question. under the patent system, taxation is of interest to almost everyone who plans to take advantage of this feature.

The point is that entrepreneurs such a case are freed from unnecessary paperwork. It should be noted that with a patent there are no reports. You will not have to submit an income tax return or any other documentation. Moreover, regardless of activity. The PSN does not provide for reports to the state. Many businessmen are interested in this advantage.

However, exceptions still occur. If we are talking about the provision of certain services, you will have to fill out BSO forms. This is the only documentation that exists.

Trade and PSN

Individual entrepreneurs on the patent tax system (2016 or any other year - not so important) engaged in trade also have some features. Which ones exactly?

Rather, they can be called an advantage of the chosen taxation system. It is noted that entrepreneurs may not use cash registers. But upon the buyer's request, any proof of purchase must be provided. For example, a cash receipt order.

Accordingly, even in the case of trading, you don’t have to think about reporting. This, as already emphasized, makes life much easier. The only serious paperwork is the actual registration of entrepreneurship. In Russia, nothing else special is provided for individual entrepreneurs with PSN.

Account books

However, you will have to keep some records just in case. But, as a rule, it is not included in reporting. The document in question is the accounting book. Individual entrepreneurs who use the patent tax system, like other entrepreneurs, are encouraged to record all their expenses and income in such a book. For what?

According to established laws, the patent has a limitation on annual income. They cannot exceed 60,000,000. Accordingly, the accounting book is more needed by the entrepreneur. It will help indicate that set limit not spent.

Books of income and expenses are presented only at the request of the tax authorities. And no one else. Perhaps this is the only one serious documentation that everyone faces. In practice, such paper is not requested very often.

Insurance premiums

Insurance premiums of individual entrepreneurs in the patent taxation system have their own characteristics. The document under study was originally invented to facilitate accounting and reporting. But insurance payments no one canceled. What does it mean?

The law on the application of the individual entrepreneur patent taxation system states that a citizen is not exempt from insurance premiums for a patent. This means that the entrepreneur will have to make appropriate contributions to the Pension Fund, as well as to the Federal Compulsory Medical Insurance Fund. The rule applies to individual entrepreneurs without employees, and to those who have employees under their command.

How much exactly will you have to pay? It is difficult to understand this issue. After all, deductions to Pension Fund Russia directly depends on the income of the citizen. In addition, there are minimum standard deductions. They change annually.

The situation for 2016 should be considered. So, if a citizen’s annual income does not exceed 300 thousand rubles, he will have to pay only 19,356 rubles 48 kopecks. If the profit is above the specified limit, then you will have to transfer only 1% of the difference between the real income and the previously specified limit.

You will also have to transfer to the FFOMS cash. Only it is fixed and does not depend in any way on the entrepreneur’s profit. Established by the state annually. Today, contributions to the Federal Compulsory Medical Insurance Fund amount to 3,796 rubles 85 kopecks.

Such deductions are relevant, as already mentioned, both for persons working “for themselves” and for those who hire subordinates for further work. Thus, in 2016, individual entrepreneurs pay 23,153 rubles 33 kopecks in the form of mandatory deductions to the previously mentioned bodies. There is nothing difficult or special to understand about the process.

How to open an individual entrepreneur

How can you get a patent? What will it take? Let's assume that the patent tax system will be applied in Moscow. In this case, the individual entrepreneur must collect a certain list of documents and submit them to the tax authority at the place of his registration. Moreover, regardless of the region of residence. You can contact, for example, the Federal Tax Service No. 10 of Moscow. It is located on Bolshaya Tulskaya Street 15.

The citizen must bring with him (when initially opening an individual entrepreneur with a patent):

- ID card (passport);

- registration certificate (if applicable) passport, no paper needed);

- application of the established form for opening an individual entrepreneur;

- application for transition to PSN;

- SNILS;

- a payment slip indicating payment of the state duty for starting a business.

That's all the papers requested tax authorities, are ending. It is recommended to provide all listed documents along with copies. There is no need to certify them.

Instructions for obtaining a patent for individual entrepreneurs

The last thing we recommend you pay attention to is step by step instructions upon obtaining a patent. Some entrepreneurs or future businessmen sometimes have certain difficulties with this feature. After all, the PSN provides for payment for the issued document. And when starting a business with other tax calculation systems, you just need to pay state fee for the procedure.

Accordingly, the patent taxation system for individual entrepreneurs provides next algorithm actions:

- Register an individual entrepreneur. There is nothing difficult in the process. It is enough to bring the previously listed documents to the MFC or the Federal Tax Service and receive a registration certificate.

- Take ready-made form to obtain a patent. It can be downloaded from the official website of the Federal Tax Service of the Russian Federation. Form 26.5-1 will be required.

- Complete the document. If difficulties arise, you can contact specialized assistance services for opening an individual entrepreneur and obtaining patents.

- Take the documents listed earlier, but attach to them the completed form 26.5-1, as well as a certificate of opening an individual entrepreneur.

- Submit an application of the established form to the Federal Tax Service at the place of registration of the entrepreneur. In return, the citizen will be given a receipt for new documents.

- After about 5 days, you can come to the tax authority and obtain a patent. To do this, you will need an INN, SNILS and a citizen’s passport.

- Take the details and pay for the received patent. The amount will be calculated depending on the duration of the document, as well as the region of residence of the citizen and the type of activity of the entrepreneur.

The following can be said about paying for a patent:

- It is not necessary to pay off the debt in full later than graduation validity period of the paper. The rule applies to patents issued for no more than 6 months.

- 1/3 of the cost of the patent must be paid no later than 3 months from the date of validity of the document, the rest - before the end application of PSN. Relevant for a system used for more than six months (inclusive).

Every citizen planning to open an individual entrepreneur and use a patent in conducting their activities should remember all this. As a rule, it is better to pay off the debt immediately. This will get rid of unnecessary problems and checks.

This is how individual entrepreneur registration occurs. The patent tax system is something that makes life much easier for some entrepreneurs. It's not difficult to use. The transition to such a tax calculation scheme is voluntary. No one has the right to force him. This is a free choice of some entrepreneurs.

About the cost of patents

How much will this or that patent cost? Another question that interests part of the population. After all, it is always important to understand how appropriate it is to use a particular taxation system.

Today, anyone can calculate for themselves how much a patent will cost them. In order not to delve into all the subtleties and features of the calculations, it is recommended to use special service, located on the Federal Tax Service website.

You can find a patent cost calculator on the page - patent.nalog.ru/info. Here you need to select:

- year of patent issue;

- duration of the document;

- region of residence of the citizen (region, city);

- type of activity;

- number of employees.

After entering the appropriate data, just click on the “Calculate” button. An inscription will appear on the screen with the cost of the patent, as well as instructions regarding payment for the document. Convenient, simple, fast. Every citizen is able to understand in literally a few minutes how much a particular patent will cost him, without delving into the nuances of calculating its cost.

Results and conclusions

What conclusions can be drawn? The citizen in the case under study does not have to pay any tax. The patent system initially provides only for payment of the document, as well as insurance premiums. And nothing more. This technique significantly reduces the burden on both tax authorities and entrepreneurs.

The patent system and the law on self-employment adopted in Russia help the population who do business on their own to “come out of the shadows” and earn income illegally. After all, it’s no secret that individual entrepreneurs often have a lot of paperwork, as well as various fees and taxes. Therefore, the tax system we are studying is ideal for many freelancers.

Registration, as already mentioned, does not take much time. No unnecessary documentation or need to submit accounting documents allows even a novice businessman to try himself in one or another field of activity. We can say that after paying for the patent and making insurance premiums, the citizen has every right sleep peacefully - he will no longer be in debt to the state and tax authorities. Opening an individual entrepreneur with a patent tax system is easier than it seems.

- Lipotropic products: our helpers that break down fats Lipotropic substances in which products

- Anatomy - what kind of science is it?

- The main layers in the solar atmosphere What is the visible layer of the solar atmosphere called?

- Sanitary treatment of the patient 1 sanitary treatment of the patient

- Modern dictionary of the Russian language stress pronunciation orthoepic

- The magic of numbers. Why do you dream about the Face? Dream Interpretation dirty face in the mirror

- Personal eastern horoscope

- The great mantra of Shiva - Om Namah Shivaya Shivaya namah nama om meaning

- Dream Interpretation: why you dream of walking through a cemetery, interpretation of the meaning of sleep for men and women

- Lego Secret Figure Minifigures Series 17

- Real benefits and mythical harm of dates for the human body

- Daniel Defoe "The Life and Extraordinary Adventures of Robinson Crusoe" - Document How many years did Robinson stay on the island

- What is the difference between Sunnis and Shiites

- Closing the month in accounting

- Main current account in 1s 8

- Schemes for correcting old errors

- Biography of Irina Saltykova: personal life, creativity

- Dysphoria - what is it and how is it treated?

- How to attract a Taurus man

- Gems for scales. Stones for scales. Where to wear a talisman stone for Libra women