Drawing up a balance sheet - an example for dummies

The balance sheet is the type of reporting that the legislature is required to submit to almost all enterprises. This document serves to display in the most complete format all the processes that take place within the company. We call the theoretical consideration of this process an example of compiling a balance sheet for dummies, which is what we will do in this article.

Simplified form of Balance available at .

A little theory about the balance sheet. The structure of the report is determined by two tables, one of which is called Asset, and the second - Liability.

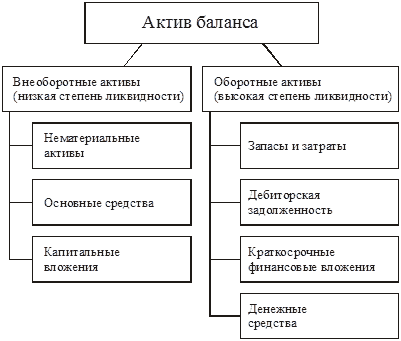

Assets

An asset includes all the possessions of an enterprise that can be converted into a monetary equivalent. This may be the premises, and equipment, and vehicles, which is owned by the company. The asset also includes those amounts that other enterprises owe to this. All elements of an asset must be displayed in monetary terms.

In simple terms, this is everything that belongs to this enterprise.

The asset has its own structure. Its fragment is non-current Assets. This is the property of the enterprise, which it uses for a long time in order to successfully carry out its business activities. This category includes buildings, equipment, vehicles, etc.

The second fragment of the structure of the Asset is the current Asset. Its final indicator is the amount of funds that are used by this enterprise for a relatively short time and require constant replenishment. This category includes materials, goods, raw materials, receivables that will return soon, etc.

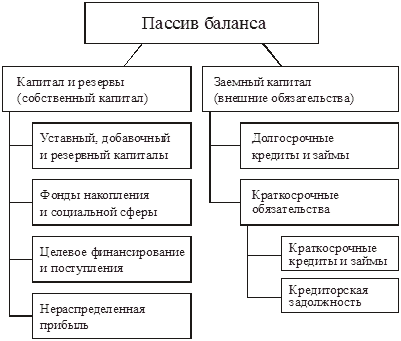

Passive

The passive is provided in order to display those sources from where the funds placed in the Asset appear. It also has its own classification and may consist of the following groups:

- raised funds (credits and loans);

- equity capital of the company;

- authorized capital;

- external liabilities (debts to suppliers, taxes, etc.)

The passive has three main structural sections:

- All funds belonging to the founders of the company or to itself are organized in the column “Capital and reserve funds”.

- The entire amount of debts that do not need to be paid in the near future, which will be paid in a period exceeding a year, form the “long-term liabilities” section.

- Wages, debts to suppliers for goods, as well as those that must be paid in the near future, form the "short-term obligations" section.

Achieving equality between is the main goal of compiling the balance sheet. It is compiled in accordance with Form 1 for the balance sheet, adopted by law for approval back in 2010. This reporting form is issued more as a recommendation document and may undergo changes related to the specifics of the organization's activities.

The essence of filling the balance sheet and instructions

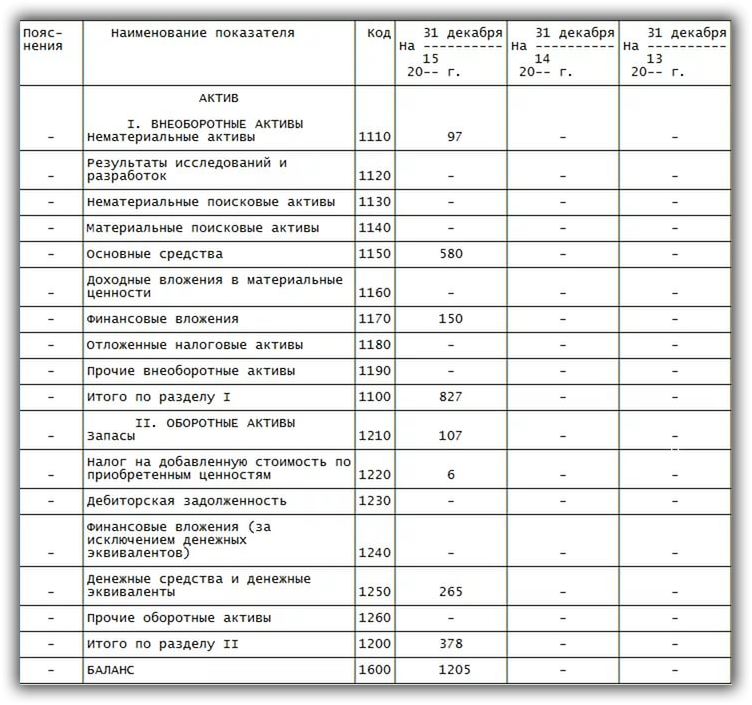

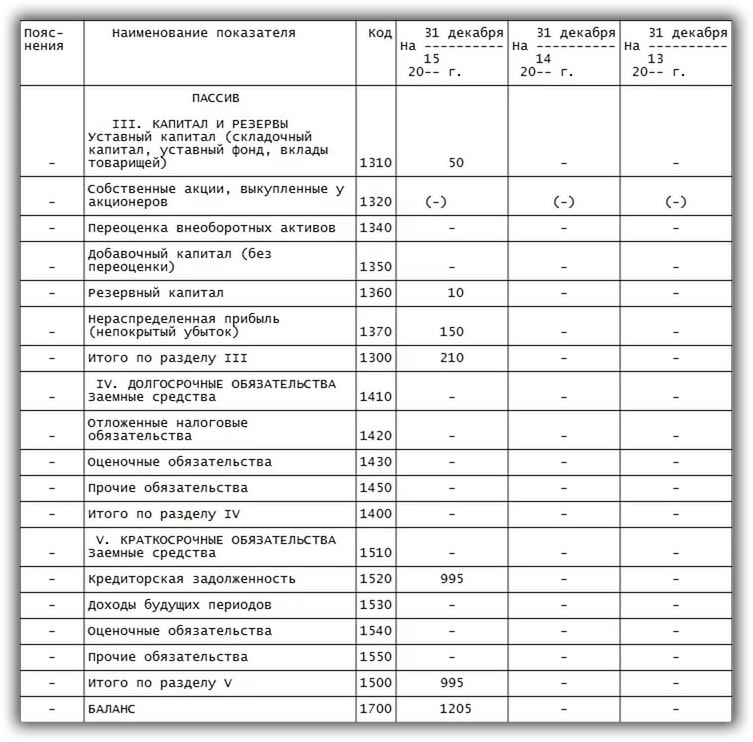

The formation of the balance sheet is carried out in the process of filling in by the entrepreneur all the lines of the form intended for this, taking into account the subtleties and nuances of the activities carried out by the company.

Both halves of the document are formed by lines, in which those indicators are entered separately that characterize the financial position of the enterprise.

Each line has its own serial number, and also shows the name of the indicator that is displayed in this line.

The total amount of the asset, taking into account the procedure for filling out the balance sheet, is found by summing up all the indicators in accordance with their sequence over the first two balance sections.

An example of filling in an Asset in the balance sheet:

An example of filling in the Liabilities of the balance:

Sometimes an amount equal to zero can be entered in some lines, then this fact should be explained in the documents accompanying the balance sheet.

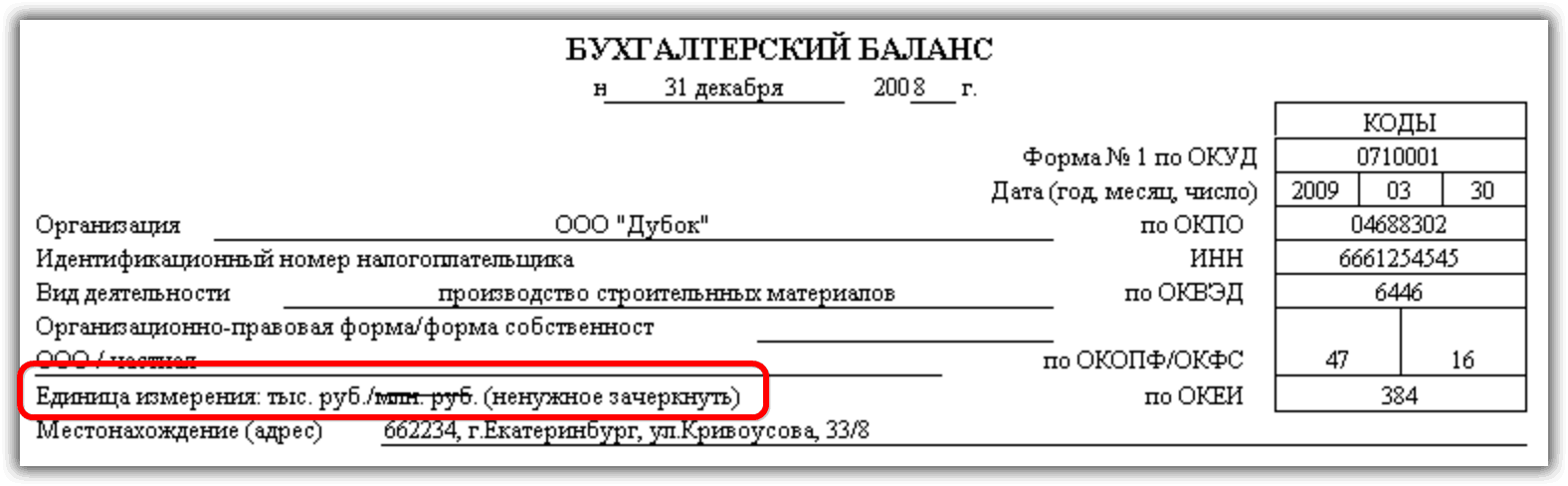

The reflection of amounts in the balance sheet takes into account the reduction of amounts by three or six zeros (in thousands or millions). So, if the value of real estate, which is in the possession of this company, is 10,000,000 rubles, then this amount can be reflected in the balance sheet as 10,000 thousand. Some companies, whose scale of activity is very large, may use their own abbreviation, which is convenient for them.

You can choose how to express the indicators when filling out the heading of the balance form:

Full instructions on how to draw up a balance for dummies can be seen in this video:

So, when answering how to draw up a balance sheet, one should consider its two main components - this is Asset and Liability, which are represented by two tables and are designed to display all financial processes occurring within the company and in its interaction with other organizations, from the point of view of the financial transaction itself, as well as its source.

- How to get a TIN via the Internet - step by step instructions

- Title page of the work book: all the nuances and sample filling

- SNILS for a newborn: instructions on how to get

- Help 3 personal income tax - what is it?

- How to fill out a cash flow statement: line by line example

- Making a cash receipt order: filling in and examples

- What documents are needed to obtain SNILS for a child

- Form AO-1. Advance report

- Rules and procedure for filling out an advance report by an accountant and accountable persons

- Help 2-NDFL sample filling

- How to fill out an application in the form No. UTII-2

- Pros and cons of ooo and ip

- Filling out the certificate 2 personal income tax - step by step instructions

- Help 2-NDFL new sample: latest changes and instructions for filling out the form

- How to write an application for another paid vacation?

- Payroll, Form T-53

- Help 2-NDFL: who should fill out, deadlines, sample filling

- How much tax does an employer pay for an employee?

- Szv m by mail

- tax deduction for children