How to fill out section 2 of 6-personal income tax: step by step instructions

In Russia, on October 14, 2015, the reporting form was approved: the calculation of personal income tax in the form of 6 personal income tax, which was calculated and withheld from individuals in the reporting period. The declaration in the approved form is required to be completed and submitted to the IFTS for all tax agents (companies, organizations, enterprises and individual entrepreneurs).

Report in the form 6-NDFL: delivery regulations, structure

A report in the form of 6NDFL is submitted to the tax office quarterly. The deadline for submission is the last day of the month following the reporting month. If this date falls on a holiday, Saturday or Sunday, then the valid date for submitting the report is the next business day after the weekend or holiday.

In 2017, the calculation according to the report must be submitted to the tax authority no later than:

- April 3, 2017 (annual calculation for 2016),

- May 2, 2017 (quarterly report for the three months of 2017),

- the thirty-first of July 2017 (semi-annual report for 2017),

- October thirty-first, 2017 (nine-month report 2017).

The report for 2017 must be submitted no later than April 2, 2018.

Violation of deadlines for submitting reports leads to sanctions from the tax authorities. The tax agent is punished with a fine of one thousand rubles for each overdue month, even if the delay was only one day.

Penalties are provided for incorrect registration and errors in the calculation of 6NDFL. For inaccuracies discovered by the tax authorities, you will have to pay a fine of five hundred rubles.

This report provides information not on a specific individual, but in general on the accrued and transferred income tax for all individuals who received income in the organization.

The calculation of accrued and withheld amounts in the 6NDFL report has the following composition:

- basic information about the tax agent: title page

- total estimates: section 1

- detailed information: section 2

It is important to know the rules for the formation of section 1, how to fill out section 2 of the 6 personal income tax report, title.

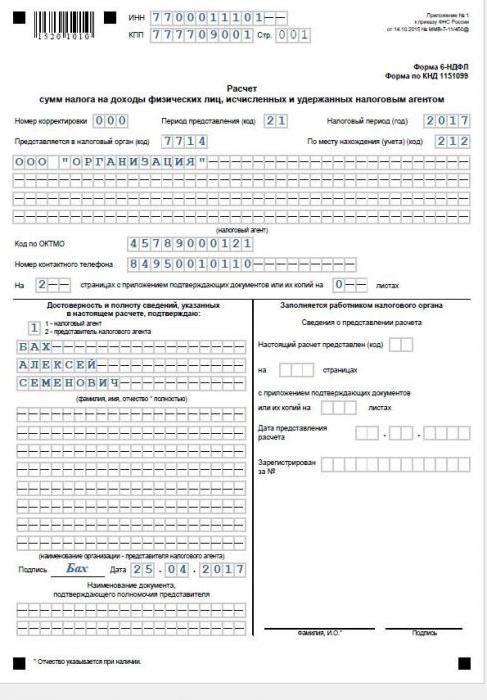

6NDFL report: title

On the first (title) page are indicated:

- registration data of the tax agent (name with decoding, OKTMO code, TIN, KPP, contact phone number);

- information about the submitted report (name of the form, CND code, submission code and year of the tax period);

- information about the IFTS).

The title page is certified by the head or his representative.

An example of filling out sheet No. 1 (title) is given below.

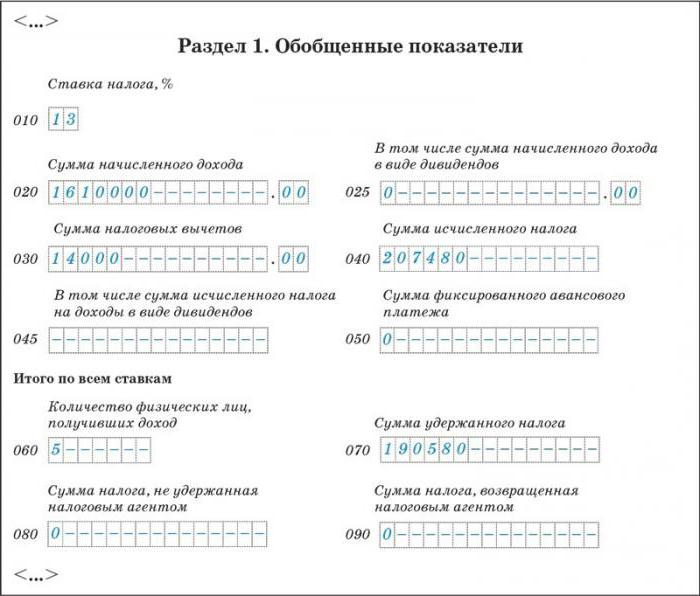

Form 6 personal income tax: totals

General indicators for calculating and withholding personal income tax in the reporting period are indicated in the first section.

Section 1 is prescribed for each rate at which income tax was calculated. Typically, the company applies a rate of 13 percent.

Separately, for each rate, the first section shows data for the reporting quarter, calculated on an accrual basis for the entire tax period:

- the total amount of calculated income (together with dividends) and separately the amount of dividends;

- applied tax deductions (total amount);

- the amount of income tax calculated, withheld, not withheld, returned by the employer;

- the number of employees (individuals who received taxable income).

Attention: as a rule, the amount of income tax calculated is not equal to the amount withheld. The actual withholding of income tax is made on payment for the month and often falls on the month of the next reporting period.

A sample of filling out section 1 of the report 6 of the personal income tax is given below.

The values of the indicators of the first section depend on how to fill out section 2 of section 6 of the personal income tax.

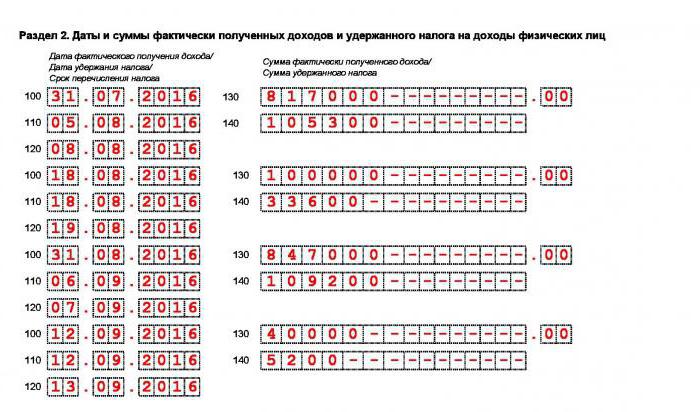

Second section 6 personal income tax: basic details

2 section 6 personal income tax - information table. It lists in chronological order:

- all transactions for accrual of income that were paid in the reporting period (during the quarter) with the obligatory indication of the date of accrual;

- the amount of income tax withheld from each income paid, indicating the date of withholding;

- the actual date of transfer of income tax to the IFTS.

Information on each income received in the second section of the form is indicated in blocks:

- date and amount of income actually received by employees - gr. 100 and gr. 130 respectively;

- date and amount of tax withheld (from the amount indicated in column 130) - column. 110 and gr. 140 respectively;

- the deadline for transferring income tax to the budget (for this type of income) - gr. 120.

2 section 6 of personal income tax (sample filling in accounting) is presented below.

Basic rules for filling out the second section of 6NDFL

Cash benefits paid in the reporting quarter, but not subject to income tax, are not shown in the report.

In the form of 6NDFL, the amount of income before tax is entered, that is, it is not reduced by the amount of income tax.

The information provided in the second section of the form does not match the information in the first section. Since the first section provides the cumulative results of the entire tax period, including the reporting quarter, and the second - the data of only the reporting quarter.

If on the same day incomes were received that have different deadlines for payment to the budget, then in the form they are indicated in different lines.

Line 120 indicates the deadlines for the transfer of income tax established by the Tax Code of the Russian Federation. If the tax is transferred before the deadline, in gr. 120 does not reflect the actual date of payment, but the maximum allowable TC.

It is especially necessary to be careful in a situation where the payment of income and the transfer of tax were actually made on the last day of the quarter. The date of payment of tax to the budget must be indicated in accordance with the Tax Code, and this will already be the date of the next reporting period. Therefore, a record of the transaction should be reflected in the next quarter.

If the income at the enterprise was paid only in one quarter or once a year, then the report is submitted for the quarter in which the income was paid, and without fail in subsequent quarters of the current year.

And in such a situation, how to fill out section 2 of form 6 of the personal income tax - income was paid only in the second quarter? For the first quarter, the report can not be submitted (since it is with zero indicators), the report for the second, third and fourth quarters must be submitted. In this case, only the first section is filled in the report for the third and fourth quarter.

How to fill out 6 personal income tax: lines 100-120

The information in lines 100-120 depends on the type of accrual.

A table that allows you to determine how to correctly fill out section 2 of section 6 of the personal income tax is given below.

| Type of income | date fact. payout income page 100 | Hold date income tax page 110 | Deadline for payment of income tax to the budget page 120 |

Wage, bonuses and allowances | Last day of the month accrued wages | Payday | Next day after day enumerated or payment at the payroll |

Holidays, pay unemployed sheets. | Vacation pay day and payment of leaflets is not difficult capabilities | holiday pay day, and pay bills disability | Afterbirth. day of month payout holiday pay and unemployed sheets. |

final settlement when leaving from worker | day of dismissal | End of payment day dismissal calculation. | Next day for pay day final settlement |

income in kind. | Income Transfer Day in kind. form | close payment date other income | Next day for pay day income |

| Per diems over the limit | Afterbirth. day of the month into a cat prepared advance report | nearest payment day other income | Next day for pay day income |

material benefit from economy on the % | Last calendar. day of the month on which the contract is valid | Next issue date other income | Next day for issuance of income |

Etc. non-wage income | Day received income remuneration | Day received income remuneration | The day following earning income, remuneration |

Reward on service agreement contractor | Day listed. to personal account or cash advance remuneration contractor | Day of transfer or issuance of cash. remuneration | Next for payment reward day |

Drawing up the second section of 6NDFL: data for the report

How to fill out section 2 6 personal income tax? The calculation is presented according to the initial data of Lampochka LLC.

In the fourth quarter In 2016, 14 individuals received income at the enterprise:

- twelve people working under labor contracts;

- one founder of LLC (not an employee of Lampochka LLC);

- one designer working in an LLC under a civil law contract for the provision of services.

The company employs people who are entitled to standard income tax deductions.

Two employees during 2016 were provided with standard:

- Petrova N.I. - within 10 months from the beginning of the year for 1 child 1400 rubles x 10 months = 14,000 rubles

- Morozov E.N. - within 3 months from the beginning of the year for three children - ((1400 x 2) + 3000) x 3 months. = 17,400 rubles

- During 2016, one employee was provided with a standard deduction as a disabled person: Sidorov A.V. - for 12 months from the beginning of the year, the deduction amounted to 500 x 12 months. = 6000 rubles.

In order to easily fill out section 2 of the calculation of 6 personal income tax for the fourth quarter. 2016, we will use the following auxiliary table. It reflects the amounts of payments, tax deductions, accrued and paid tax in the 4th quarter.

date extradition income | date actual received (charges) income | date hold personal income tax | date re number personal income tax | Afterbirth deadline day listed personal income tax | Receive type remuneration (income) in rubles | Sum income in rubles | Sum tax deductions in rubles | withheld personal income tax in rubles |

| 11.10.16 | 30.09.16 | 11.10.16 | 11.10.16 | 12.10.16 | Salary for September (end. | 300000 | 1900 | ((300000+150000) 58253, where 150000 already paid advance for 1 half september |

| 20.10.16 | 31.10.16 | 11.11.16 | 11.11.16 | 12.11.16 | 150000 | |||

| 20.10.16 | 20.10.16 | 20.10.16 | 31.10.16 | 31.10.16 | unemployed | 24451,23 | ||

| 25.10.16 | 25.10.16 | 25.10.16 | 25.10.16 | 31.10.16 | Reward under contract prov. services | 40000 | ||

| 11.11.16 | 31.10.16 | 11.11.16 | 11.11.16 | 14.11.16 | Salary second floor. | 317000 | 1900 | ((317000+150000) |

| 11.11.16 | 11.11.16 | 11.11.16 | 30.11.16 | 30.11.16 | Vacation | 37428,16 | ||

| 20.11.16 | 30.11.16 | 09.12.16 | 09.12.16 | 12.12.16 | Salary pay for the first half | 150000 | ||

| 30.11.16 | 09.12.16 | 09.12.16 | 12.12.16 | Salary for the second half | 320000 | 500 | ((320000+150000) |

|

| 20.12.16 | 30.12.16 | 11.01.17 | 11.01.17 | 12.01.17 | Salary for the first floors. December | 150000 | ||

| 26.12.16 | 26.12.16 | 26.12.16 | 26.12.16 | 27.12.16 | Dividends | 5000 | ||

| 27.12.16 | 27.12.16 | 27.12.16 | 27.12.16 | 28.12.16 | Gifts in not monetary form | 35000 | 910((35000-28000) |

|

| TOTAL | 1528879,39 | 194560 | ||||||

The table shows New Year gifts given to seven employees.

In 2016, these employees did not receive material assistance and other gifts.

An example of filling out the second section of 6NDFL

According to the information indicated in the table above, we will consider how to fill out section 2 6 of the personal income tax:

First block:

- line 100 - 30.09.2016 line 130 - 300000;

- p. 110 - 11.10.2016 p. 140 - 58253;

- pp. 120 - 10/12/2016.

Second block:

- line 100 - 20.10.2016 line 130 - 24451.23;

- p. 110 - 20.10.2016 p. 140 - 3183;

- pp. 120 - 31.10.2016.

Third block:

- pp. 120 - 31.10.2016.

Fourth block:

- line 100 - 25.10.2016 line 130 - 40000;

- pp. 110 - 25.10.2016 pp. 140 - 5200;

- pp. 120 - 31.10.2016.

Fifth block:

- line 100 - 31.10.2016 line 130 - 317000;

- p. 110 - 11.11.2016 p. 140 - 60463;

- pp. 120 - 11/14/2016.

Sixth block:

- p. 100 - 11.11.2016 p. 130 - 37428.16;

- p. 110 - 11.11.2016 p. 140 - 4866;

- pp. 120 - 11/30/2016.

Seventh block:

- line 100 - 30.11.2016 line 130 - 32000;

- p. 110 - 09.12.2016 p. 140 - 6103;

- pp. 120 - 12.12.2016.

Eighth block:

- line 100 - 26.12.2016 line 130 - 5000;

- pp. 110 - 26.12.2016 pp. 140 - 650;

- pp. 120 - 27.12.2016.

Ninth block:

- line 100 - 27.12.2016 line 130 - 35000;

- pp. 110 - 27.12.2016 pp. 140 - 910;

- pp. 120 - 12/28/2016.

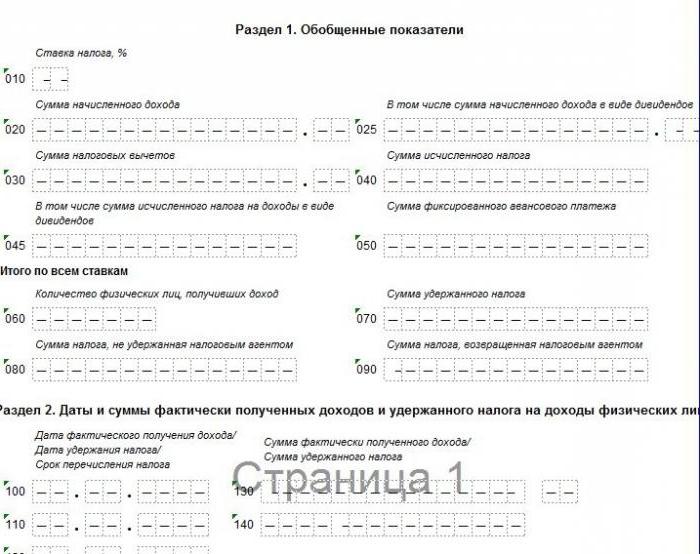

2 section 6 personal income tax: form, sample filling out a zero report

The 6NDFL report is required to be submitted by tax agents: enterprises (organizations) and individual entrepreneurs that pay remuneration for work to individuals. If during the calendar year an individual entrepreneur or an enterprise did not accrue or pay income to employees and did not conduct financial activities, then the zero calculation of the 6NDFL form can not be submitted to the IFTS.

But if an organization or individual entrepreneur provides a zero calculation, then the IFTS is obliged to accept it.

The inspectors of the IFTS do not know that the organization or individual entrepreneur did not conduct financial activities and were not tax agents in the reporting period, and are waiting for a calculation in the form of 6NDFL. If the report is not submitted within two weeks after the deadline for submission, then the IFTS has the right to block the bank account and impose penalties on the individual entrepreneur or organization that did not submit the report.

In order to avoid trouble with the IFTS, the accountant has the right to provide a 6NDFL declaration (with empty values) or write an information letter to the IFTS.

A sample of a report prepared for delivery with zero indicators is given below.

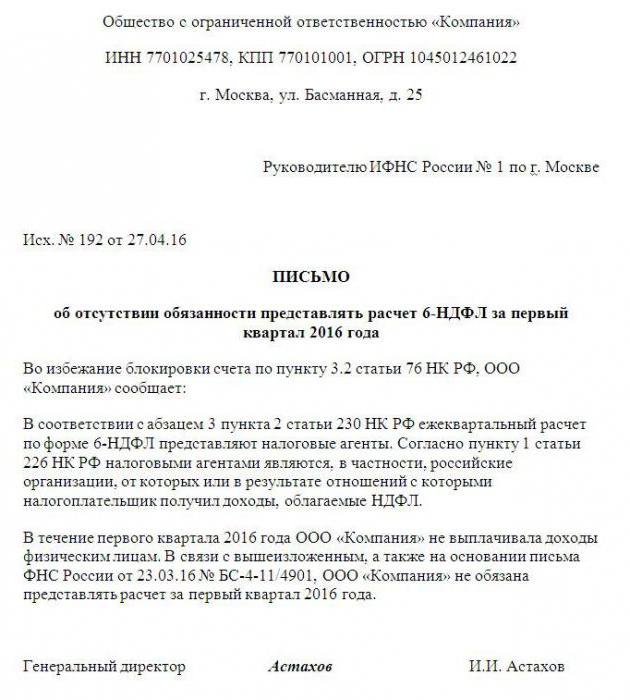

A sample letter to the IFTS about a zero report can be seen below.

Filling in 6 personal income tax: an algorithm of actions

To facilitate the work of filling out the second section of the calculation of 6NDFL, you must:

- Collect all payment orders for the payment of personal income tax in the reporting quarter.

- Select all payment orders for the transfer of income to employees and cash receipts for the issuance of income from the cash desk, arrange them in chronological order.

- Create an auxiliary table according to the example described above

- Fill in the information for each type of income in the table according to the information given in the section: "How to fill out 6NDFL: lines 100-120".

- From the completed auxiliary table, take information for section 2 of the calculation of 6 personal income tax.

Attention:

- Line 110 indicates the day on which the employee's income was actually paid (even if the salary or other income was paid later than the date established by the Tax Code).

- Personal income tax is not withheld when paying an advance.

- In line 120, the deadline for transferring tax to the budget by type of income is entered, and not the actual date of transfer of income tax (even if the tax is transferred later than the date established by the Tax Code).

- In line 140, the amount of the calculated income tax from the paid income is entered (if the income tax is not transferred in full or not transferred at all, then the tax that should have been transferred is still entered).

The second section 6 personal income tax. Situation: Impossible to withhold tax

How to fill out section 2 of 6 personal income tax when it is not possible to withhold income tax from an employee?

An individual received income in kind (for example, a gift), but in the future he has no cash payments.

The employer does not have the opportunity to withhold and transfer to the budget income tax from income given in kind.

How to fill out section 2 of 6 personal income tax in this situation is indicated below:

- line 100 - day of issuance of income in kind;

- p.110 - 0;

- p.120 - 0;

- line 130 - income in kind (amount);

- p.140 - 0.

The amount of unwithheld income is indicated in the first section of the declaration on page 080.

Conclusion

Declaration 6 personal income tax - a new report for accountants. When filling it out, a large number of questions arise, not all the nuances are considered and reflected in the recommendations given by the tax authorities. Explanations and clarifications on controversial issues are regularly given in official letters from the Federal Tax Service of the Russian Federation. In 2017, there are no changes to the reporting form and the rules for filling it out. This article reflects how to fill out section 2 of section 6 of personal income tax in the most common situations, the above algorithm for compiling the second section of the calculation is successfully applied in practice.

Good luck with your reporting!

- How to get a TIN via the Internet - step by step instructions

- Title page of the work book: all the nuances and sample filling

- SNILS for a newborn: instructions on how to get

- Help 3 personal income tax - what is it?

- How to fill out a cash flow statement: line by line example

- Making a cash receipt order: filling in and examples

- What documents are needed to obtain SNILS for a child

- Form AO-1. Advance report

- Rules and procedure for filling out an advance report by an accountant and accountable persons

- Help 2-NDFL sample filling

- How to fill out an application in the form No. UTII-2

- What circumstances will help reduce the fine in the FSS

- Chip tuning equipment - flashing secrets Difficulties associated with chip tuning

- Chiptuning for beginners

- Appeal, sample appeal against the decision of the arbitration court Sample appeal to the arbitration court

- Characteristics in the military registration and enlistment office for a school student, writing rules

- Ready-made examples (samples) of characteristics for secondary school students

- Characteristics for a student from school to the military registration and enlistment office

- Appointment of an agreement for the repayment of debts and drafting a document Debt Management Agreement

- How to learn to sell a product?